The fund that has the lowest average expense ratio from the given options is an Indexed fund.

<h3>Why are expense ratios for Indexed funds so low?</h3>

Index funds are funds that invest on a particular index such as the S&P 500 Index which follows the 500 companies on the S&P.

The way these funds work is by investing on a certain index entirely and then leaving the investment to run on its won based on the returns of the index that was invested in.

Because these funds just follow an index, they do not need people to monitor them and make analysis that will lead to higher returns for investors.

As a result of this, the overhead attached as a result of wages for analysts is reduced. With the total expenses being reduced, so also will the average expense ratio.

In conclusion, the fund that generally has the lowest average expense ratio is the indexed find.

Find out more on indexed funds at brainly.com/question/7804398

#SPJ1

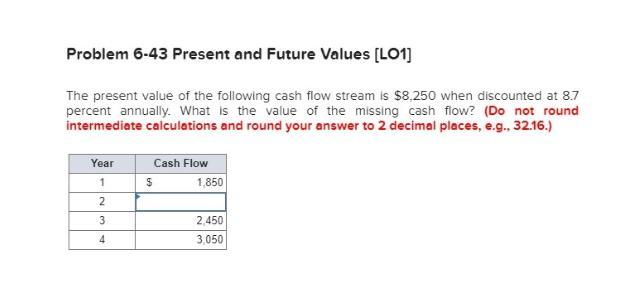

Answer:

The question is not complete,find attached complete question.

The missing cash flow is $2,901.77

Explanation:

In order to calculate the missing cash flow, I discounted the other cash flows given to present values using the formula PV=FV/(1+r)^n as is it in the attached spreadsheet.

Thereafter , I equated the present values to the total present value of $8250 given using X for the unknown cash flow, by solving this equation I arrived at the present value of the missing cash flow .

Finally, I multiplied the present value of the missing cash flow with its discounting factor of 1.1816 , hence I arrived at the missing cash flow of $ 2,901.77

Net income is the amount that will be earned after all the taxes have been subtracted from the paystub amount.

<h3>

The net income for the paycheck</h3>

Given Information:

- Paycheck=$329.40

- Paystub=$400.00

- Medical tax=$5.80

- Social security tax=$24.80

- Federal tax=$40.0

The Net income is therefore:-

Net Income=Paystub-Medical tax-Social security tax

Net Income= 400 - 5.80 - 24.80 - 40

Net Income= $329.40

In conclusion, the net income is $329.40.

Learn more about Net income, refer to the link:

brainly.com/question/20938437

Answer:

B) The State Disability Insurance (SDI) program benefits received for a period of disability are not taxable as income, but benefits received for time off under the Paid Family Leave program are federally taxable as income.

Explanation:

Disability insurance benefits are not reported for tax purposes with one exception. If a person are receiving unemployment insurance benefits,

become unable to work due to a disability, and begin receiving disability insurance benefits, your disability insurance benefits are considered a substitution for your unemployment insurance benefits, and will then be reported for tax purposes.

If disability insurance benefits are reported, a notice will accompany the first benefit payment sent to you advising that the benefits are being reported to the Internal Revenue Service. The employment development department will provide you with a 1099G tax form in January showing the reported amounts paid and forward a copy to the Internal Revenue Service.

Paid family leave benefits are reported for federal purposes but not state tax purposes.

Paid family leave benefits are not taxable or reported to the California State Franchise Tax Board.

Answer:

An advantage gained by spreading fixed production costs over a large production volume.

Explanation:

Economies of scales refer to that scale where the larger quantity of an output having similar level fo fixed cost cause in less cost per unit. It could be occured from an advantage that could be benefit by distributing the fixed production cost over and above to the wider production volume

Therefore the above statement should be considered