Answer:

3. Expected inflation rate

Explanation:

To determine the amount of money that the medical student must invest today to meet this capital need, she needs to know the current cost of medical equipment to have the the amount she needs to be able to buy the equipment. Also, she has to know the assumed rate of return to determine the amount of interest she will receive as the formula to calculate the money she needs today is:

PV= FV/(1+r)^n, where:

PV= present value

FV= future value

r= rate of return

n= number of periods of time

According to this, the answer is that the option that she doesn't need to find the amount of money that must be invested today to meet this capital need is the expected inflation rate as the formula to calculate the present value considers the amount she will need, the rate of return and the period of time.

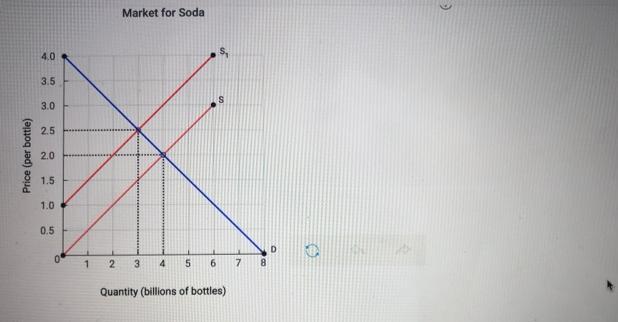

Answer: hello your question is poorly structured attached below is the missing graph and missing part of the question

Assume the government imposes a $1.00 excise tax on the sale of every 2 liter bottle of soda. The tax is to be paid by the producers of soda. The figure below shows the annual market for 2 liter bottles of soda before and after the tax is imposed.

answer :

a) $2 , 4 billion

b) $2.5

c) $1.5

d) 3 billion

e) $3 billion

Explanation:

a) equilibrium price = $2 per bottle

equilibrium quantity = 4 billion bottles

<u>b) After imposition of excise tax </u>

consumers will pay = $2.5

<u>c) The amount producers keep after the imposition of taxes </u>

= $2.5 - tax

= 2.5 - 1 = $1.5

<u>d) New equilibrium quantity ( after tax is imposed ) </u>

= 3 billion bottles ( from graph attached ) i.e. intersection of S2 and D

e)<u> Amount of tax revenue collected by the government from the imposition of tax </u>

= quantity of bottles sold * $1

= 3 billion * $1 = $3 billion

Answer:

6.67 solution: Actual labour hour=8hr total no.of employees=4 Total working

Explanation:

<span>This is part of the concept of involvement. Being involved in the hunting sport makes sure that people are responsible for their actions in the future, makes people aware of the needs and requirements of those who do undertake the activity, and gives people the information they'll need in order to be successful at the activity.</span>

Explanation:

An intrinsic reward is an intangible award of recognition, a sense of achievement, or a conscious satisfaction. For example, it is the knowledge that you did something right, or you helped someone and made their day better.