The amount they can take as deduction for the loss on the sale of their home is; $0.

<h3>How much can they take as deduction for the loss on the sale?</h3>

It follows that deductions can only be taken on losses incurred on the sale of property used for business or investment purposes.

Hence, since the item sold is their personal home, it follows that they cannot take any deduction on the loss on the sale.

Read more on sale deduction;

brainly.com/question/22525377

#SPJ1

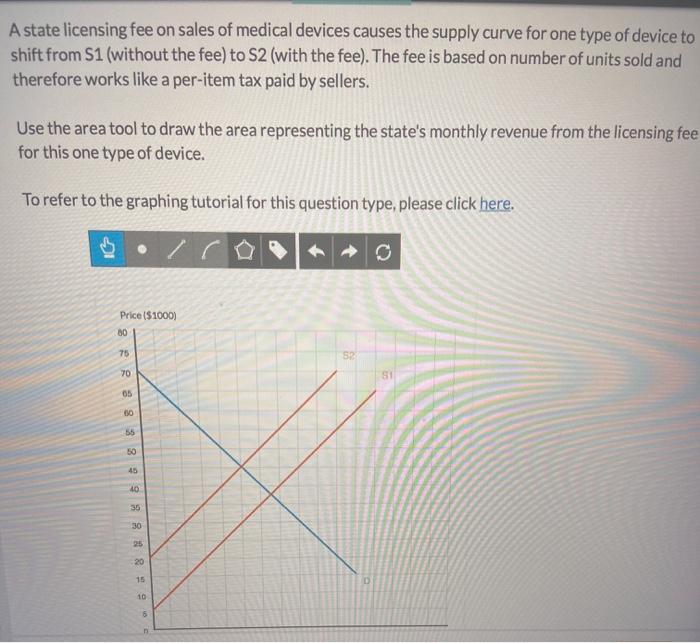

Answer: hello your question is incomplete attached below is the complete question

answer ; Government revenue from tax = $750,000 per month

Explanation:

Attached below is the required graph

Government revenue from tax ( per month )

= ( 450 - 30 ) ( 50 - 0 )

= $750,000 per month

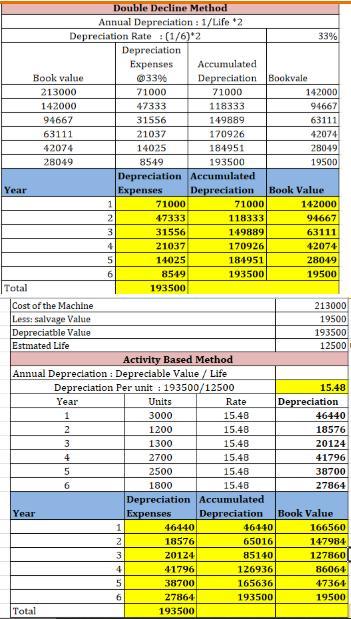

Answer:

The depreciation schedule for six years is attached below.

Explanation:

Answer:

True

Explanation:Information policy can be seen a singular set of policies made public by an organization to make sure that all her IT users in the domain or network of the organization comply with guidelines and regulation related to the protection of the information stored online/digitally at any point within the organization's boundaries of authority or in the network.

Answer:

The disadvantage of using range is:

Explanation:

It not measure the spread of the majority of values in a data set (only measures the spread between highest and lowest values).