Answer:

a. When marginal cost is above average cost, average cost is rising; but when marginal cost is below average cost, average cost is falling.

b. The lowest point at which a plant or firm can produce such that the long-run average cost of the plant or firm is at the minimum.

c. The average total cost curve (ATC) U-shaped in the short run because of diminishing returns.

d. The average total cost curve (ATC) is U-shaped in the long run because economies of scale and diseconomies of scale.

e. The shape of the average variable cost curve (AVC) is usually U-shaped or upward-sloping; while the shape of the average fixed cost curve (AFC) is a Rectangular Hyperbola.

Explanation:

a. What is the relationship between the marginal cost of production and average total cost of production?

Marginal cost refers to the change in total cost when extra unit of output is produced, while average cost is the total cost divided by the number of units produced.

The relationship between the two is that when marginal cost is above average cost, average cost is rising; but when marginal cost is below average cost, average cost is falling.

b. What is efficient scale of production?

Efficient scale of production can be described as the lowest point at which a plant or firm can produce such that the long-run average cost of the plant or firm is at the minimum.

c. Why is the average total cost curve (ATC) U-shaped in the short run?

The average total cost curve (ATC) U-shaped in the short run because of diminishing returns.

Diminishing returns occur when the amount of a single factor of production is incrementally increased while holding all other factors of production constant, the marginal output of a production process decreases.

d. Why is the average total cost curve (ATC) U-shaped in the long run?

The average total cost curve (ATC) is U-shaped in the long run because economies of scale and diseconomies of scale.

Economies of scale can be described as a situation whereby increasing output leads to lower long-run average total costs.

But, after a given level of output, scale diseconomies may be encountered by a firm.

Diseconomies of scale can be described as a situation whereby increasing output leads to higher long-run average total costs.

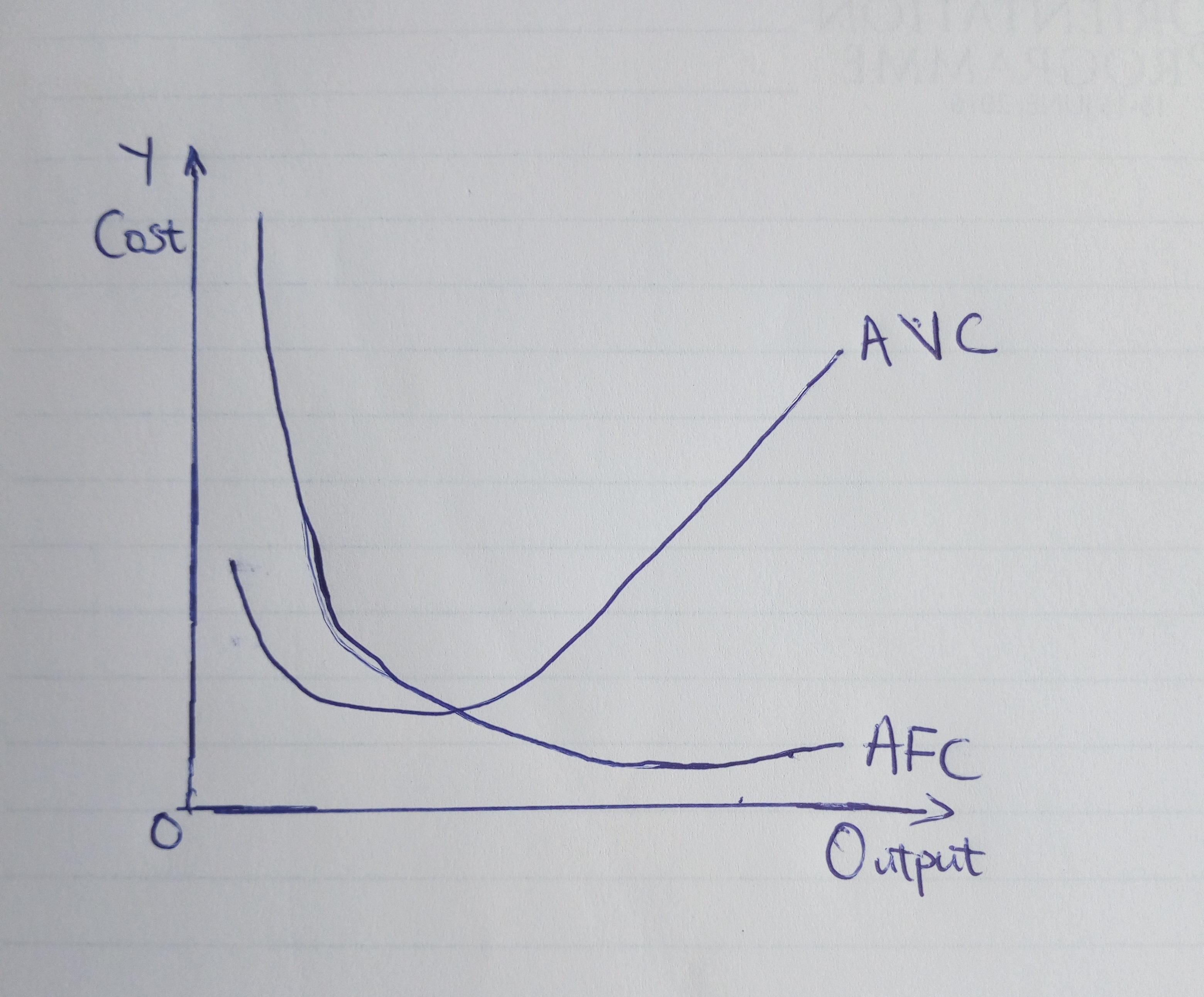

e. What are the shapes of the average variable cost curve (AVC) and the average fixed cost curve (AFC)?

Note: See the attached photo for the curves of the AVC and AFC showing their shapes.

The shape of the average variable cost curve (AVC) is usually U-shaped or upward-sloping.

The shape of the average fixed cost curve (AFC) is a Rectangular Hyperbola. This occurs because the same amount of fixed cost is split by increasing output. Therefore, the AFC curve slopes downwards and is a rectangular hyperbola, meaning that the area under the curve is constant at all places.