Answer: 0

Explanation:

Firstly, we will calculate the nominal value in 2015 which will be:

= $500 x 1 million

= $500 million

The nominal value in 2016 will be:

= $1000 x 1 million

= $1 billion

Real GDP will be the price of the base year multiplied by the quantity of the current year which will be:

= $500 million x 1 million sets

= $500 million

Therefore, the increase in real GDP is zero.

Answer:

The principle in Law 'Nemo dat quod non habet' states that an individual connot give what he does not have

Indeed Tom can rescind the contract with Matthew as he possesses voidable title to the balls

Explanation:

Until consideration has moved from Matthew to Tom the validity of the agreement/Contract remains inconclusive.

Considering his Account is not funded means he has no valid title to the Balls, he is merely in possession of the Balls but not the Owner.

Tom can sue demanding a return of the Balls irrespective of Matthew having sold them to Aaron.

Another illustration could be given of a thief who sells off a property. Inspite of the Buyer being unaware, because the thief has a voidable title it makes the transaction invalid.

The complete question is as follows:

What percentage of your gross salary does the consumer financial bureau suggest?

The proportion of gross income suggested by the Consumer Financial Bureau is not more than 15% or 10% of the earned income.

<h3>What is a gross salary?</h3>

Gross salary is the amount received by an employee before any deductions and income taxes. It is given by the employer of the company in its respective bank account.

According to the Consumer Financial Bureau, the proportion of not exceeding 10% of gross income should be reserved for affording the student loan payments, or not greater than 15% be reserved for monthly debts except rental and mortgage reimbursements.

Therefore, the type of payments will decide the proportion of gross income being allocated in accordance with the Consumer Financial Bureau.

Learn more about the gross salary in the related link:

brainly.com/question/5715627

#SPJ1

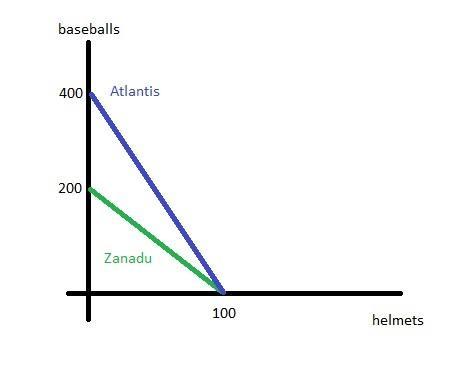

Answer:

a) see attached image

b) Atlantis's opportunity cost of producing one helmet = 200 / 100 = 2 baseballs

c and d) Atlantis's opportunity cost of producing one baseball = 100 / 200 = 0.5 helmets

Zanadu's opportunity cost of producing one baseball = 100 / 400 = 0.25 helmets ⇒ Zanadu has a comparative and absolute advantage in the production of baseballs

e) yes, Atlantis would produce 100 helmets, and if it trades 50 to Zanadu, it will get 150 baseballs in return. So it will gain from trade. If Zanadu produces 400 baseballs and trades 150 of them for 50 helmets, it will also benefit.

Explanation:

B, sole proprietor. It couldn't be the others.