Answer:

The income before tax is $370450, the income tax is $111135 and the net income is $259315.

Explanation:

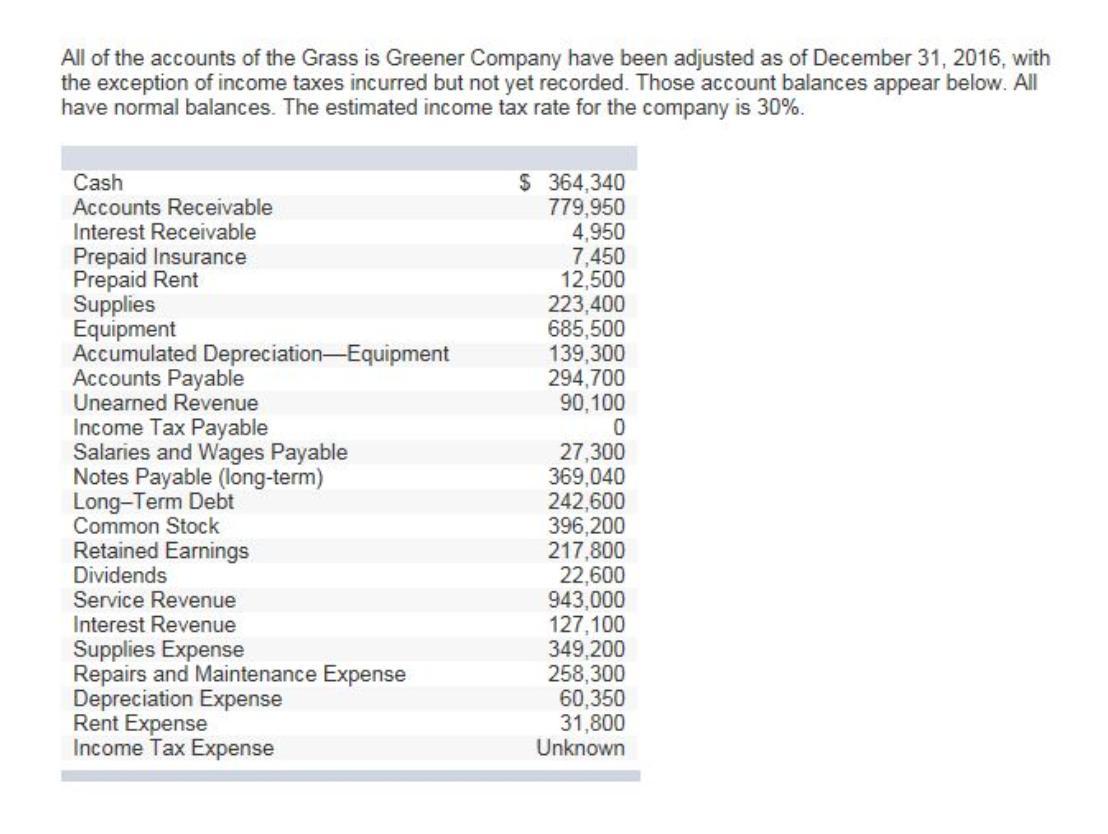

As the data table is not visible,online a similar question is found for which the data is attached here with.

From the given data

Service Revenue=$943,000

Interest Revenue=$127,1000

Total Revenue=Service Revenue+Interest Revenue=$1070100

Now The expenses are given as

Supplies Expense=$349,200

Repairs and Maintenance Expense =$258,300

Depreciation Expense=$60,350

Rent Expense=$ 31,800

Total Expense=Supplies Expense+Repairs and Maintenance Expense+Depreciation Expense+Rent Expense=$699650

So the income before tax is given as

Income=Total Revenue-Total Expense

Income=$1070100-$699650

Income=$370450

So the income before tax is $370450.

Now the tax is estimated at 30% as given tax rate as

Tax=Rate*Income

Tax=30%*$370450

Tax=$111135

So the income tax is $111135.

Now the Net income is given as

Net Income=Income-Tax

Net Income=$370450-$111135

Net Income=$259315

So the Net Income is $259315.