Answer:

Check the explanation

Explanation:

This question is connected to the company's gross manufacturing margin and it can be calculated by taking away or subtracting the cost of goods sold from the overall amount of sales or revenue. The result will then be divided by the entire revenue or sales to arrive at the gross margin.

800-520=280

280/800=0.35=35%

Since the question says you have $1,000 to spend or save you have to put what are the risks, advantages and disadvantages you might have with a,b,c and d

Answer: d) "The advantage of radioactive iodine is that I will not need future medication for my disease."

Explanation:

The treatment of Graves disease using radioactive iodine is meant to destroy the thyroid gland so that the person will see a reduced function from it.

This means that after the treatment is used, a lot of patients will need a thyroid replacement and will have to keep receiving treatments to maintain.

Essentially the radioactive iodine is not the last medication that will be taken for Graves disease.

Answer:

0.5

Explanation:

A portfolio has 21% standard deviation

The return is 16%

T-bills were paying 5.5%

Therefore the Sharpe ratio can be calculated as follows

= 16-5.5/21

= 10.5/21

= 0.5

Hence the Sharpe ratio is 0.5

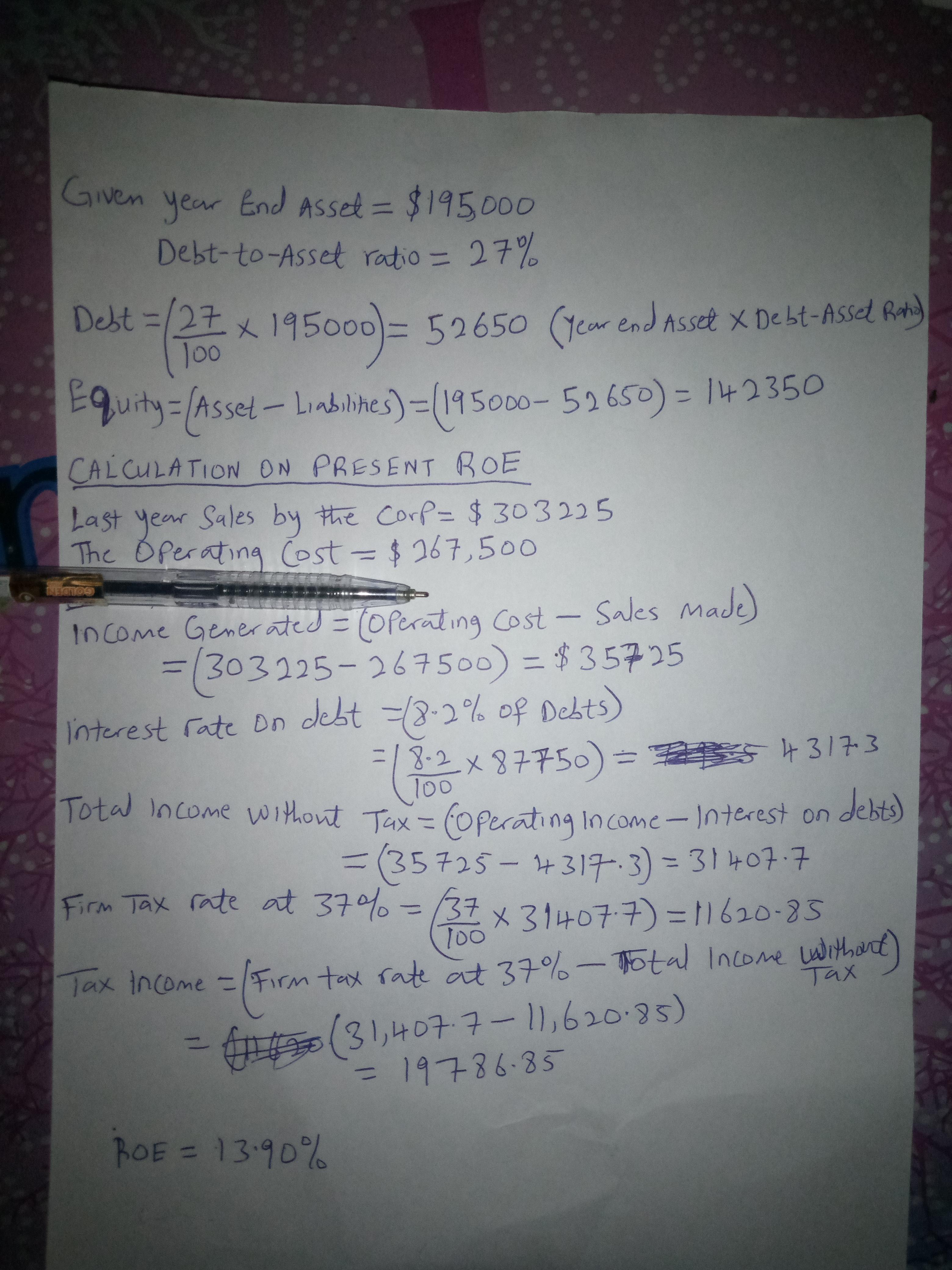

Answer:

The correct option is D

There is increase in ROE by 2.86%

d. 2.86%

EXPLANATION:

THIS IS THE COMPLETE QUESTION BELOW;

Last year Swensen Corp. had sales of $303,225, operating costs of $267,500, and year-end assets of $195,000. The debt-to-total-assets ratio was 27%, the interest rate on the debt was 8.2%, and the firm's tax rate was 37%. The new CFO wants to see how the ROE would have been affected if the firm had used a 45% debt ratio. Assume that sales and total assets would not be affected, and that the interest rate and tax rate would both remain constant. By how much would the ROE change in response to the change in the capital structure?

a. 2.08%

b. 2.32%

c. 2.57%

d. 2.86%

e. 3.14%

CHECK THE ATTACHMENT BELOW FOR DETAILED EXPLANATION