Answer:

corruption is the root of social ills because those that are in power take money for their own use and that money was supposed to buy medication for the country

The two measures which can be used by Nando’s to assess environmental turbulence within the macro-environment are predictability and changeability.

<h3>What is an

environmental turbulence?</h3>

An environmental turbulence can be defined as a measure of the rate and unpredictability of changes that occurs in a business firm's external environment.

In this context, we can infer and logically deduce that the two (2) measures which can be used by Nando’s to assess environmental turbulence within the macro-environment are predictability and changeability.

Read more on environmental turbulence here: brainly.com/question/20377406

#SPJ1

<span>The company is using market-penetration pricing.</span>

Answer:

Total cash collections in February are $133600

Explanation:

The collections in the month of February will include 20% of sales made in February in account for cash sales.

Cash sales = 140000 * 0.2 = $28000

Thus, Credit sales for February are = 140000 - 28000 = $112000

Out of these credit sales made in February, 60% will be collected in February. Thus, credit sales made in February that will be collected in February are,

February collections from February credit sales = 112000 * 0.6 = $67200

Total cash collections in February from February sales = 67200 + 28000

Total cash collections in February from February sales = $95200

In addition, out of the credit sales made in January, 40% will be collected in February.

Collection from January sales in February = 120000 * 0.8 * 0.4 = $38400

Total collections in February = 38400 + 95200 = $133600

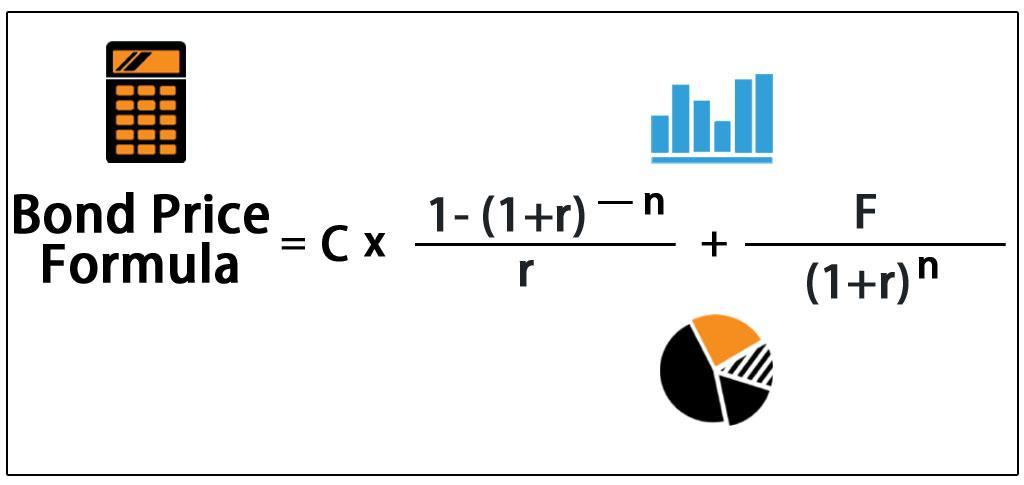

Answer:

Bond Price = $875.6574005 rounded off to $875.66

Explanation:

To calculate the price of the bond today, we will use the formula for the price of the bond. We assume that the interest rate provided is stated in annual terms. As the bond is an annual bond, the coupon payment, number of periods and annual YTM will be,

Coupon Payment (C) = 1,000 * 0.05 = $50

Total periods (n) = 3

r or YTM = 0.10

The formula to calculate the price of the bonds today is attached.

Bond Price = 50 * [( 1 - (1+0.10)^-3) / 0.10] + 1000 / (1+0.10)^3

Bond Price = $875.6574005 rounded off to $875.66