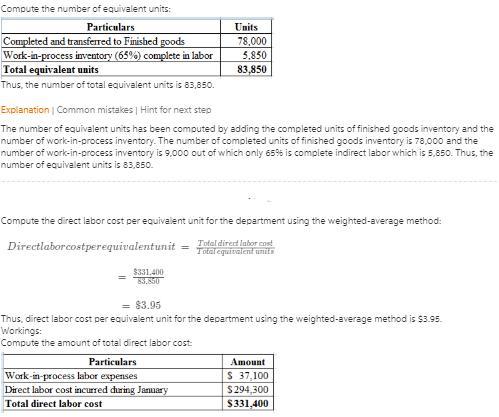

Answer:

The direct labor cost per equivalent unit for the department using the weighted-average method is $3.95.

Explanation:

Detailed steps are given below.

Answer:

Earnings per share 2016 = $0.00073

Earnings per share 2017 = $0.00095

Explanation:

Earnings per share relates to a period and not for a particular date, therefore, it is computed based on the average number of shares for the period.

Net income for each year

2017 = $62,000

2016 = $50,700

Shares at the end of year

2017 = 64,507,000

2016 = 66,282,000

2015 = 73,139,000

Average shares of 2016 =

Average shares of 2017 =  = 65,394,500

= 65,394,500

Earning per share for 2016 =

Earnings per share for 2017 =

Answer:

B. $2 per unit

Explanation:

The computation of the price of Y is shown below:

As we know that the condition of the utility maximization i.e ratio of Marginal utility and the price should be matched and equal for both the goods given in the question

For one good

= Marginal utility ÷ price

= 40 ÷ $5

= 8

And, for the other goods

Marginal utility ÷ price = 8

16 ÷ Price = 8

So, the price is $2 per unit

Hence, the correct option is B.

Answer:

P0 = $137.2988907 rounded off to $137.30

Explanation:

The two stage growth model of DDM will be used to calculate the price of the stock today. The DDM values a stock based on the present value of the expected future dividends from the stock. The formula for price today under this model is,

P0 = D0 * (1+g1) / (1+r) + D0 * (1+g1)^2 / (1+r)^2 + ... + D0 * (1+g1)^n / (1+r)^n + [(D0 * (1+g1)^n * (1+g2) / (r - g2)) / (1+r)^n]

Where,

- g1 is the initial growth rate

- g2 is the constant growth rate

- D0 is the dividend paid today or most recently

- r is the required rate of return

P0 = 2 * (1+0.15) / (1+0.07) + 2 * (1+0.15)^2 / (1+0.07)^2 +

2 * (1+0.15)^3 / (1+0.07)^3 +

[(2 * (1+0.15)^3 * (1+0.05) / (0.07 - 0.05)) / (1+0.07)^3]

P0 = $137.2988907 rounded off to $137.30