Answer:

the firm's cost of debt financing = 6.682 %

Explanation:

Given that:

St. Thomas Company is planning to issue $1,000 par value bonds.

Bond coupon rate = 9.5

which will be sold at $980

Floating cost = 1 - 4 % of the market value

The bonds will mature in 15 years and coupon payments will be semi-annual .i.e Period = 15 × 2

Marginal tax rate = 35%

The objective is to determine the firm's cost of debt financing

From the information given ; we can use the EXCEL Spreadsheet to compute the value for the cost of debt then after that we will be able to find the firm's cost of debt financing.

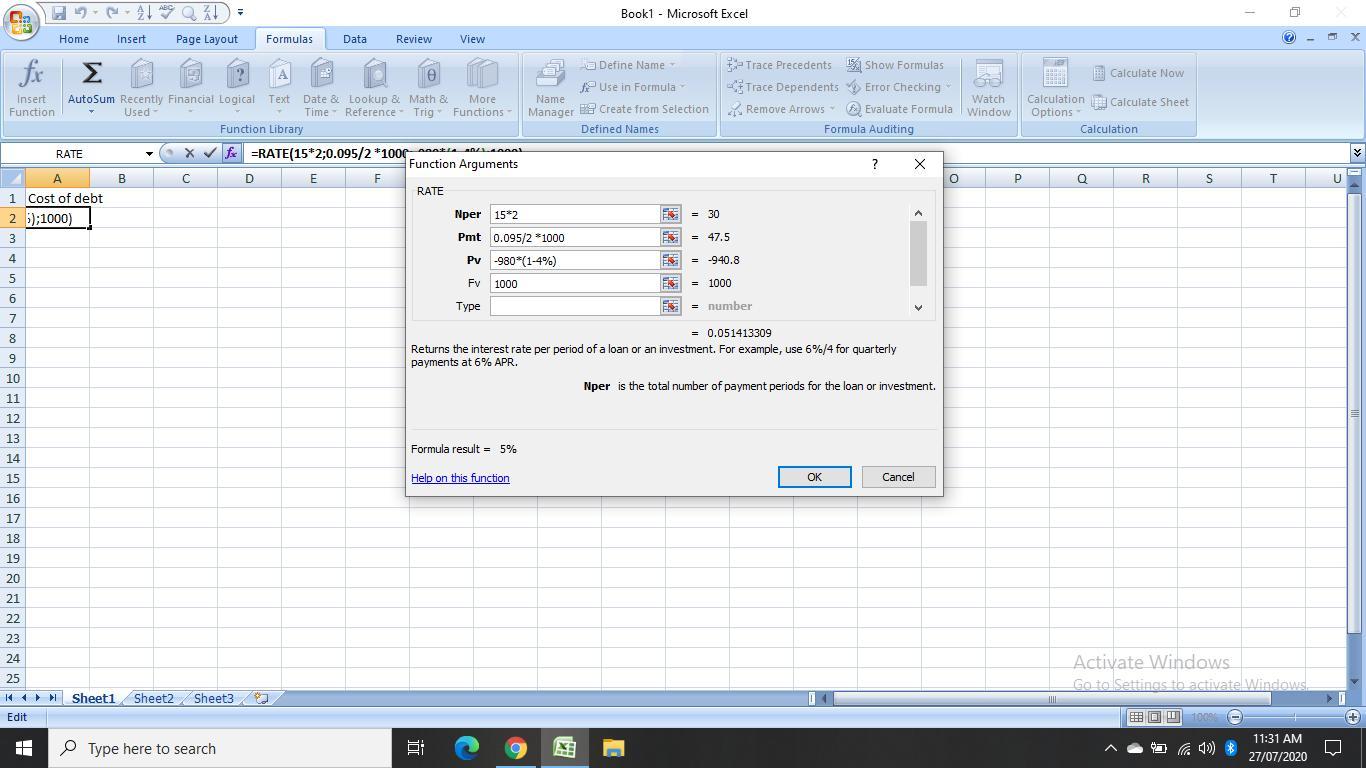

The following data will be inserted into the Excel function (=RATE(15*2;0.095/2 *1000;-980*(1-4%);1000) )

Future value Fv= 1000

Payment Pmt =0.095/2 *1000

number of period Nper= 15 × 2

Present value Pv= -980 × (1 - 4%)

Output = 0.051413309  5.14%

5.14%

The Screenshot of the Excel Computation is also shown in the attached file below.

Pre tax cost of debt = 2 × cost of debt

Pre tax cost of debt = 2 × 5.14% = 10.28%

FInally ;

the firm's cost of debt financing = Pre-tax cost of debt × (1 - Tax rate)

where the marginal tax rate = 35%

the firm's cost of debt financing = 10.28% × (1 - 35%)

the firm's cost of debt financing = 0.1028 ×( 1 - 0.35)

the firm's cost of debt financing = 0.1028 × 0.65

the firm's cost of debt financing =0.06682

the firm's cost of debt financing = 6.682 %