Answer:

See calculations below

Explanation:

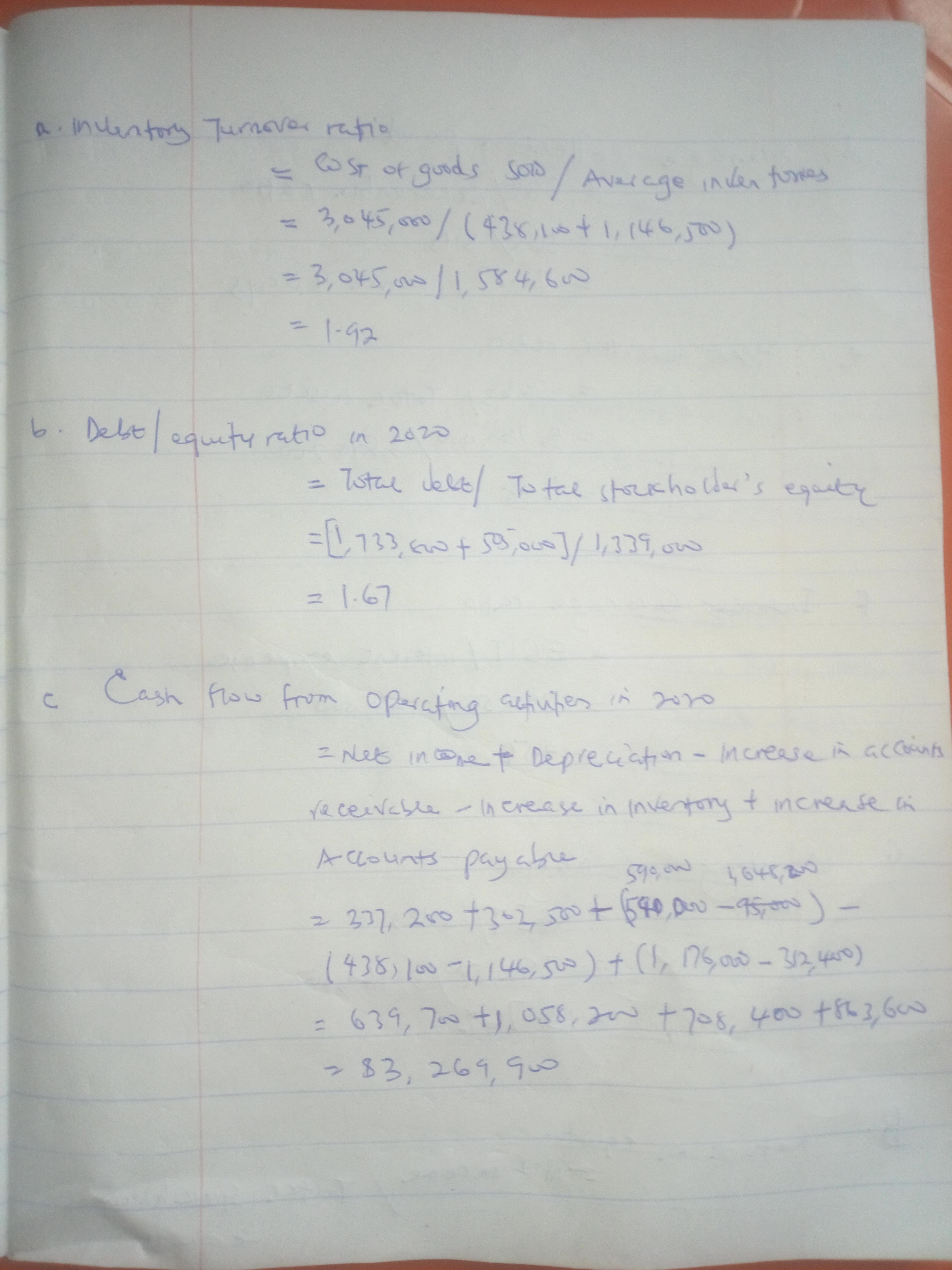

a. Inventory turn over ratio = 1.92

b. Debt equity ratio = 1.67

c. Cash flow from operating activities in 2020 = $3,269,900

d. Average collection period = 71 days

e. Asset turnover ratio = 1.48

f. Interest coverage ratio = 4.56

g. Operating income = 13.76%

h. Return on equity = 25.18%

j. Compound leverage ratio = 2.27

K. Net cash provided by operating activities = $3,269,900

Please see the whole breakdown in the attached