Answer: The answer is as follows:

Explanation:

M1 = Currency with public + Checkable deposits + Other deposits with RBI

M2 = M1 + Post office savings deposits

Currency held by the public and Checkable deposits are the components of M1.

Whereas savings deposits, Money market mutual funds held by individuals and Small time deposits are the components of M2.

We know that all the components of M1 are also the components M2.

∴ The items are included in the M2 money supply but not the M1 money supply are as follows:

Item 1 - Money market mutual funds held by individuals

Item 2- Savings deposits, including money market deposit accounts

Item 5 - Small time deposits

Answer:

correct option is D). $454,513

Explanation:

given data

Annuity = $2000

rate = 7.5 % = 0.075

time period = 40 year

solution

we get here Future value of annuity that is express as

Future value of annuity = Annuity ×  ......................1

......................1

here r is rate and t is time period so now put value and we get

Future value of annuity = $2000 ×

Future value of annuity = $454513.03

so correct option is D). $454,513

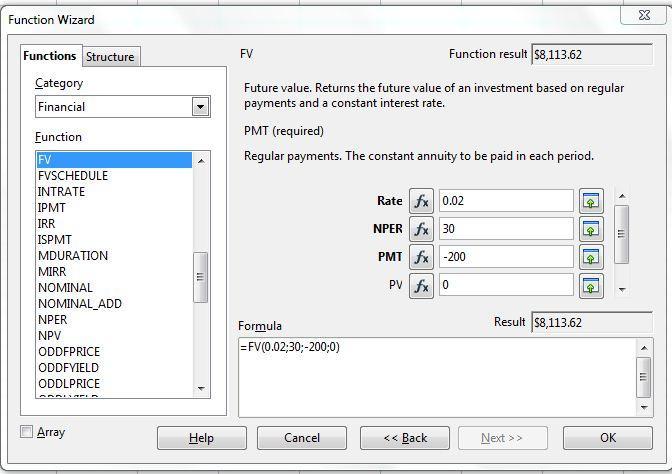

Answer:

Amount in savings account after 7 and a half years is $8,113.62

Explanation:

Given:

Quarterly payments made in savings account (pmt) = $200

Annual interest rate = 8%

Quarter interest rate (rate) = 8÷4 = 2%

Compounding period (nper) = 7 and a half years or 7.5×4 = 30 quarterly payments

This is an annuity as uniform amount of $200 is deposited every quarter.

Savings at the end of seven and a half years mean future value of annuity.

Future value of annuity can be computed using spreadsheet function =FV(rate, nper,pmt,PV)

Savings account will have $8113.62 at the end of seven and a half years.