Answer:

c. Decrease liabilities and increase revenues

Explanation:

The correct adjusting journal entry which shall be recorded by the Duluth Co. in accounts in respect of advance income as as at December 31, is given below:

Debit Credit

Advance income(Liability) $2,000

($6,000/6*2)

Revenue $2,000

Since the liability has been debited in the above mentioned journal entry, which mean that it has been decreased and the revenue has been credited, which means that it has been increased.

So based on the above discussion, the answer is c. Decrease liabilities and increase revenues

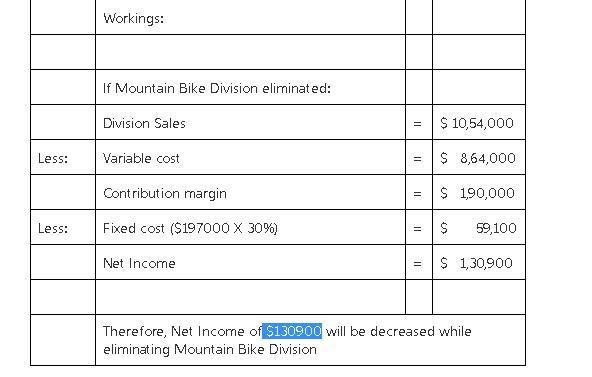

Answer:

A net income decrease of $130900 will occur by eliminating the mountain bike division.

Explanation:

Find the attachment

The answer is true

hope i helped

The answer is: C.accrual basis of accounting

Accrual basis of accounting would record a certain transaction as soon as it happen, even though an exchange of payment has not been made. Compared to any other basis, accrued basis tend to the most likely to represent the actual financial condition of a company. This is why this basis is used as the current industry standard.

Answer: Option C

Explanation:

A. Achievement of organizational goals is the result for which the controlling process is initiated.

B. Taking corrective action is the second last step in controlling process.

C. Controlling process starts with the establishment of standards from which the actual performance will be compared.

D. Comparison is the second step in controlling process.

E. Identification will be done only after the comparison and detection of deficiencies in the process.