Answer:

$59.36

Explanation:

Given that

Dividend per share = $1.30

Growth rate for next 3 years is 15%

Now

Dividend for year 1 is

= Dividend per share × (1 + growth rate)

= $1.30 × (1 + 0.15)

= $1.495

For dividend for year 2 is

= Dividend for year 1 × (1 + growth rate)

= $1.495 × (1 + 0.15)

= $1.719

For dividend for year 3 is

= Dividend for year 2 × (1 + growth rate)

= $1.719 × ( 1 + 0.15)

= $1.977

And,

Subsequent Growth rate = g2 = 5%

Now

Dividend for year 4 is

= Dividend for year 2 × (1 + g2)

= $1.977 × (1 + 0.05)

= $2.076

Now

As per Gordon's Growth Rate Model

Price at year 3 is

= Dividend for year 4 ÷ (required rate of return - g2)

= $2.076 ÷ (0.08 - 0.05)

= $69.2

So, Value of the Stock is

= Dividend for year 1 ÷ (1 + required rate of return ) + Dividend for year 2 ÷ (1 + required rate of return)^2 + Dividend for year 3 ÷ (1 + required rate of return)^3 + Price at year 3 ÷ (1 + required rate of return)^3

= $1.495 ÷ (1+0.08) + $1.719 ÷ (1+0.08)^2 + $1.977 ÷ (1+0.08)^3 + $69.2 (1 + 0.08)^3

= $59.36

Answer:

Results are below.

Explanation:

Giving the following information:

Sales $382,500 (units 5,100 $75 per unit)

variable costs $245,000 (48.04 per unit)

fixed costs $98,000.

Option 1:

Increase selling price by 16%.

New selling price= 75*1.16= 87

Sales= 5,100*87= 443,700

variable costs= (245,000)

fixed costs= (98,000)

Net income= 100,700

2. Reduce variable costs to 59% of sales.

Contribution margin= (382,500*0.41)= 156,825

fixed costs= (98,000)

Net income= 58,825

T<u>he most profitable option is the first one.</u>

Answer:

A target customer profile is simply a specific group of customers most likely to respond positively to your promotions, products, and services. 4 points regarding the nature of target customers:

- What kind of people we’re looking?

- Where to find them?

- What our customers want from our brand, to adapt our value proposition so that our brand is relevant to a specific need or problem?

- How they compare and choose products to adjust marketing campaigns to make our offering seem the most compelling?

Digital marketing has led to the growing importance of ‘Persuasive function of Promotion' because customers can learn about promotions from home and even compare the campaigns.

Explanation:

Persuading function of Promotion is to motivate customers to buy products under promotion due to intense competition among different industries producing similar types of products.

I think the answer is TASTE or PREFERENCE of the consumer or buyer.

There are 5 determinants of demand. These are:

1) price

2) price of related goods

3) income of buyer

4) taste or preference of buyer

5) expectations

The "made in the USA" is a type of branding that will influence buyer's taste or preference. There are a lot of inference about when goods are tagged as "made in USA".

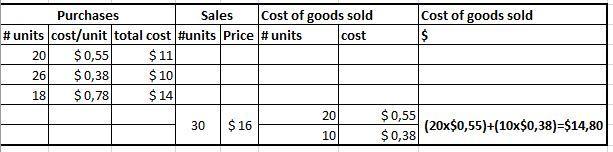

Answer:

30 units at a cost of $14,80

Explanation:

The table shows purchases sales and balance with its corresponding number of units and cost. Before Patricia sold 30 units, she had 64 units available but not all of them cost her the same. The FIFO inventory method is "First in First out" which means Patricia is going to sell the first units she bought, if she needs more then she goes to the second purchase and so on.

So, if she sold 30 unit then she is going to use the first 20 units she bought at 11$ ($0,55 per each unit), but she is missing 10, then, she is going to take 10 units from the second purchase of 26 units at $10 ($0,38 each unit).

To know the cost of goods sold we need to multiply each unit sold by its cost per unit:

20 units x $0,55 = $11

10 units x $0,38= $3,8

Then we add:

$11+$3,8= $14,80. This is the total cost of goods sold (if we assume $ 11 was the total cost for 20 units and $10 was the total cost for 26 units)