Answer:

$80 per unit

Explanation:

Data provided in the question:

Per unit selling cost of the product = $150

Per unit variable cost of the product = $70

Total fixed cost per month = $1200

Now,

The unit contribution margin is calculated as:

unit contribution margin = Selling price per unit - Variable cost per unit

Thus,

unit contribution margin = $150 - $70

or

unit contribution margin = $80 per unit

Hence,

The correct answer is option $80 per unit

Answer:

The answer is: A) Is the law rationally related to a legitimate government interest?

Explanation:

A legitimate government interest applies when a government (in this case municipal government) passes a law to protect the health, safety, and economy of it's citizens.

This law will probably be reviewed using a rational basis, which is the least strict type of legal scrutiny.

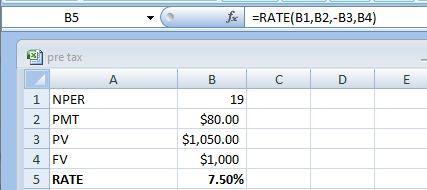

Answer:

5.925%

Explanation:

For computing the cost of debt, first we have to determine the YTM by using the Rate formula that is shown in the attachment

Given that,

Present value = $1,050

Assuming figure - Future value or Face value = $1,000

PMT = 1,000 × 8% = $80

NPER = 20 year - 1 year = 19 year

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after solving this,

1. The pretax cost of debt is 7.50%

2. And, the after tax cost of debt would be

= Pretax cost of debt × ( 1 - tax rate)

= 7.50% × ( 1 - 0.21)

= 5.925%

Answer:

Natural experiment

Explanation:

Natural experiment is the study of empirical, which comprise of the individuals who are exposed to the control as well as the conditions of the experimental , which are determined or evaluated by the nature or through other kinds of factors that are outside the person control.

The procedure of governing the exposures resemble the random experiment. This experiment are not controllable and are the observational studies. So, the event is naturally occurring, then it is an example of the natural experiment.

Answer:

How you become a good Project Manager?

You become a good project manager by making a good ans sound decision, able to work under pressure with little or no supervision, explore opportunities and have an astute skill to lead.

How to manage projects in a complex society?

Managing projects in a complex society entails keeping to time and delivering on time too. By so doing, more projects comes in as no one desire a delay in business and handling of his projects.

How to manage people to ensure a successful project team?

Good and prompt supervision making, conducting trainings to equip staff to be able to deliver the exact requirement to make business smooth.

How to understand the context of complexity of your project?

As no one jumps into becoming a project manager, it requires a process in which the operation and handling of challenges in a projects is known. Understanding the complexity of projects requires studying the projects knowing the cost and in total wha