The universe .

The Big Bang theory if the thought to be the creation of everything

Answer:

i) the intercept is - 124.84 and it is negative because when the income of individuals is zero their consumption = - 124.84 (i.e. consumer borrows 124.84 ).

ii) $25465.16

iii) attached below

Explanation:

Given that the equation is

^cons = -124.84 + .853 * inc

<u>i) Interpret the intercept in this equation and comment on its sign and magnitude</u>

intercept : the intercept is - 124.84 and it is negative because when the income of individuals is zero their consumption = - 124.84 (i.e. consumer borrows 124.84 ).

The slope = .853 is positive because consumption is will increase by 0.853 whether the income rises or decreases by the value of 1

<u>ii) Determine the predicted consumption when family income = $30000</u>

^cons = -124.84 + 0.853 * ( 30000 )

= 25465.16

hence when family income = $30000 the predicted consumption = 25465.16

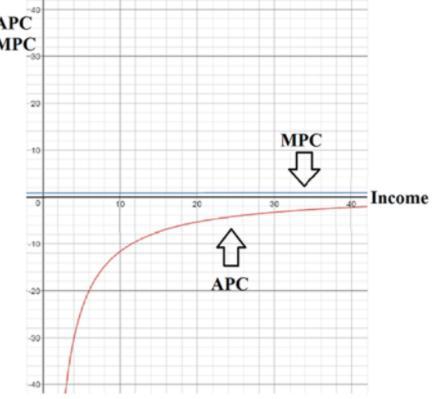

<u>iii) Draw a graph of the estimated MPC and APC ( inc on the x-axis )</u>

MPC = 0.853 ( constant )

APC = Cons / inc

attached below is the required graph

Answer:

The total cost of the units completed and transferred out of the department was: $324,900

Explanation:

First Calculate Total Cost per Equivalent Unit

Materials $2.00

Conversion $3.70

Total $5.70

Then, Calculate the Cost of Units Completed and Transferred

<em>Units Completed and Transferred × Total Cost per Equivalent Unit</em>

57,000 × $5.70

$324,900

Answer:

Fly Corporation

The stock price will not be affected by the accounting change.

Explanation:

This opinion is based on the assumption that the capital markets are efficient. Therefore, the stock's market price will reflect all available and relevant information. Since all the necessary information is already incorporated into the stock price, the CEO of Fly Corporation cannot beat the market by the change in accounting method, and the stock price will not be undervalued or overvalued. Moreover, the change in accounting method only shifts the timing for reporting income.

It's all depends on from where you are shipping the furniture from