The Rust Belt became an industrial hub due to its proximity to the Great Lakes, canals, and rivers, which allowed companies to access raw materials and ship out finished products. These were the most important factors.

Answer:

The demand curve for steel to shift to the right

Explanation:

The question isn't complete. The full question can be found: https://www.chegg.com/homework-help/questions-and-answers/3-plastic-steel-substitutes-production-body-panels-certain-automobiles-price-plastic-incre-q31436687

Substitutes goods are goods that can be used in place of one another. If the price of plastic increases, consumers shift to steel, its demand increases and the supply curve shifts to the right.

I hope my answer helps you

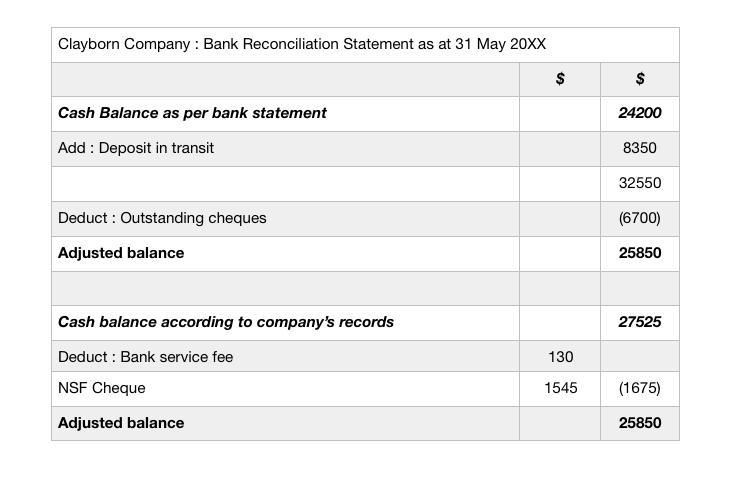

Answer:

Adjusted cash balance : $25850

Explanation:

The goal of a reconciliation statement is to ascertain the differences between the banks records and the depositor’s records and make accounting changes as deemed appropriate. There is a general flow that is used to make the correcting entries:

1. The process flow starts with the bank’s ending cash balance

2. Add any deposits made by the company to the bank that are in transit

3. Deduct any cheques that are uncleared by the bank

4. Add or deduct any other differences available as necessary

5. In the company bank records, once again start with the ending balance

6. Add interests earned

7. Deduct any bank service fees, penalties and NSF (Non-Sufficient Funds) cheques.

8. Add or deduct any other differences available as necessary

At the end of this process, it is likely that both accounts would be equal and tally.

Please refer attached table for details on the calculation.

Answer:

32.03%

Explanation:

Data provided as per the question

Net operating income = $42,930

Average operating assets = $134,000

The computation of return on investment (ROI) is shown below:-

Return on investment =net operating income ÷ average operating assets

$42,930 ÷ $134,000

= 32.03%

Therefore for computing the return on investment we simply divide average operating assets by net operating income.

<span>within 180 days from the time the employee filed a complaint provided the eeoc finds that there has been discrimination

C.

</span>