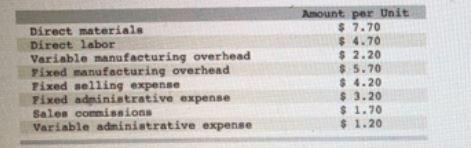

Based on the details given, the following are true:

- 1. Incremental manufacturing cost = $14.60

- 2. Incremental cost = $17.50

<h3>Incremental manufacturing cost if production increased from 20,250 to 20,251</h3>

The fixed cost will not change as the production amount is still below 24,500 units. Incremental manufacturing cost will therefore be:

= Direct material + Direct labor + Variable overhead

= 7.70 + 4.70 + 2.20

= $14.60

<h3>Incremental cost for increased from 20,250 to 20,251</h3>

This will include all costs that are not fixed.

= Incremental manufacturing cost + Sales commissions + Variable admin expense

= 14.60 + 1.70 + 1.20

= $17.50

Find out more on incremental manufacturing cost at brainly.com/question/8527680.

Answer:

The answer is B.Personal needs.

Explanation:

Bank reconciliation refers to looking at your bank statement and your personal register and making sure they match up with no discrepancies. In this case, there were discrepancies, $150 worth so John had to look and see what was missing and making sure they both equaled the same amount. From the numbers given, John's bank account was reconciled $150.

The term " Push Communication "describes the information that is sent to recipients without their request via reports, e-mails, faxes, voice mails, and other means.

<h3>

What is the difference between pull and push communication?</h3>

When an urgent reaction is not needed, push communication is appropriate. On receiving the message, the addressee does something, though. Informational communication is a type of pull communication. The message is communicated by the sender via websites, bulletins, etc.

In push communication, the sender pushes information in one direction to the receiver. The most frequent use of it is to provide expected, non-urgent information. Push communication is typically communicated in writing and does not require a prompt reaction from the recipient.

Learn more about Push Communication here:

brainly.com/question/13653950

#SPJ4

Answer:

B. auditor

Explanation:

The work of an auditor and that of the forensic accountants are very similar. They both examine financial records and statements of an organization to confirm their accuracy. The auditor and forensic accountant are specialized officers. They have been trained to detect fraudulent reporting in financial statements. After evaluating the books of account, they form an opinion based on their findings.