Answer:

(a) Firms could possibly respond to unions demands for higher wages by hiring fewer workers.

(b) Firms could possibly respond to unions demands for higher wages by substituting capital for labor.

Explanation:

Unions are formed to work toward better working conditions and welfare of staff.

Workers act collectively to negotiate better terms of employment with the employers.

However when unions try to negotiate for increased pay the employer may take different actions that will bad for the employee.

The employer may decide to actually pay the higher wage but hire fewer workers. This is usually the case when higher wages for many employees will result in loss for the employer.

Secondly the employer may substitute capital for labour. For example investing more in use of machines and reducing labour.

From the employer's viewpoint this will result in lower labour cost due to higher wage payment

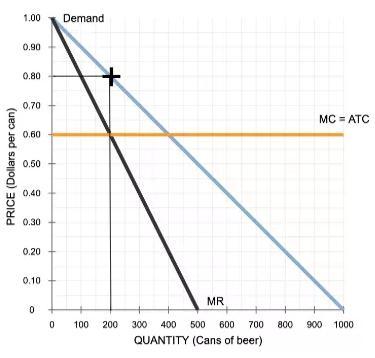

The profit-maximizing price and combined quantity of output is indicated in the demand curve by using a black point (plus symbol).

<h3>What is a cartel?</h3>

A cartel can be defined as a formal agreement between two or more business firms (producers) of a particular product or service, that's formed to control production, sales and pricing in an oligopolistic industry.

At equilibrium in a cartel, marginal revenue is equal to marginal cost (MR = MC). Thus, the profit-maximizing price and combined quantity of output should be calculated from the demand curve as illustrated in the image attached below.

Read more on cartel here: brainly.com/question/15294015

#SPJ1

<u>Complete Question:</u>

Mays and McCovey are beer-brewing companies that operate in a duopoly (two-firm oligopoly). The daily marginal cost (MC) of producing a can of beer is constant and equals $0.40 per can. Assume that neither firm had any startup costs, so marginal cost equals average total cost (ATC) for each firm.

Suppose that Mays and McCovey form a cartel, and the firms divide the output evenly. (Note: This is only for convenience; nothing in this model requires that the two companies must equally share the output.)

Place the black point (plus symbol) on the following graph to indicate the profit-maximizing price and combined quantity of output if Mays and McCovey choose to work together.

Answer:

<u>C. materials requirement planning (MRP).</u>

Explanation:

It is noteworthy that throughout the discourse of Sparky Weyer, president and CEO of Minimotors, Inc. he mentions the company's material needs inorder to increase their production.

At a point he mentions that the suppliers need detailed information about when parts are needed by the company for its new machinery. Thus this is a good example of material requirement planning.

Answer:Equity multiplier=1.6

Explanation:

Debt equity ratio is given as debt/equity , Therefore

Debt = Debt equity ratio X Equity

=0.60 x $486,000

= $291,600

The Total assets given as Liability(debt+equity) will now be

=$291,600+$486,000

=$777,600.

Therefore Equity multiplier, Total assets/Total equity

=(777,600/486,000)=1.6

A company has $100,000 in assets, 1000 shares outstanding, and no debt. If EBIT is $20,000, the interest rate on debt is 10% and its tax rate is 40%, then its EPS is 12 per share.

Earning Per Share (EPS) indicates the agency's profitability by means of showing how a great deal of cash a commercial enterprise makes for each proportion of its stock. The EPS parent is determined by way of dividing the employer's net income by using its outstanding shares of common inventory. however, it's miles taken into consideration the higher the EPS quantity, the more worthwhile the employer.

To find the ESP use the formula

ESP = Net Income / Common Share O/S- Net Income = 20000 - 0 -20000 * (.40) = 12000

ESP = 12000 / 1000 = 12 per share

Therefore Earning per share is 12 per share.

Earnings Before Interest and Taxes (EBIT) is a hallmark of an enterprise's profitability. EBIT may be calculated as sales minus charges with the exception of tax and hobby. EBIT is likewise referred to as running profits, operating earnings, and income before interest and taxes.

Learn more about EBIT here brainly.com/question/14565042

#SPJ4