Answer:

A balance sheet for Weismuller publishing for December 31 2021 was prepared and recorded in the explanation section below

Explanation:

Solution

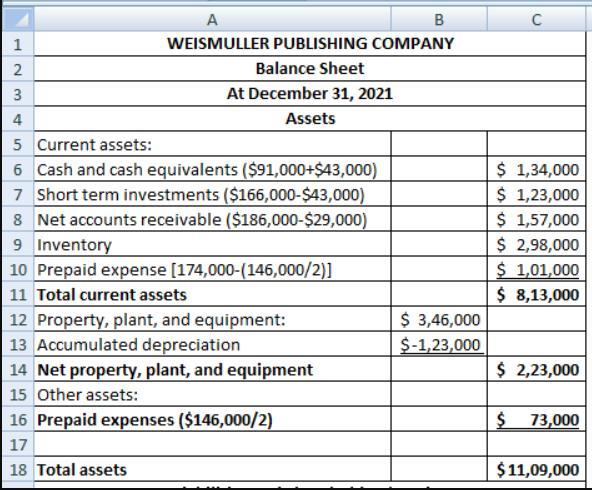

COMPANY: WEISMULLER PUBLISHING Balance Sheet At December 31 2021 Assets

Current assets:

Cash and cash equivalents ($91,000 + $43000) $134000

Short term investments ($166,000 - $43000) $123000

The net accounts receivable ($186,000 =$29,000) $175,000

Inventory $298,000

Prepaid expense [174,000-(14600/2)] $101,000

The total current assets $813,000

Note: Kindly find an attached copy of the [art of the complete solution to this question below

Use only a small percentage of your credit limit.

Generally, using more than 30% of your available credit limit can hurt your score, so only use a small percent in order to help increase it.

Answer:

Specific performance

Explanation:

Specific performance is the contract in which the party performs for the specific purpose rather than the general purpose. In this contract, one party is refusing to perform the contract due to some better options or by any other reasons

Examples - in case of real estate properties, antiques, etc.

In the given case, the contract was made for $80,000 but after two days the party deny to perform it as the party got an additional $20,000. So, this is the case of the specific performance.

<u>Ordering your latest credit report</u> is the action that appeared to be the least helpful if you’ve been the victim of identity theft. Therefore, <u>the correct answer is D.

</u>

If anyone has been a victim of identity theft, then it is important for such a person to officially report or contact any of the credit reporting companies to place a fraud alert on their credit report.

<h2>Further Explanation</h2>

Identity theft is when someone intentionally steals your information and uses such information without taking your permission. In the US, identity theft has become a booming business for fraudsters

In the US, 15.4 million Americans were a victim of theft, also identity theft tops complain of the consumer to the Federal trade commission. Regardless of how careful you seem to be, you can still fall victim to identity theft.

If you are a victim of identity theft, there are things you do immediately.

Some of the steps you can take to prevent an identity thief to further commit fraud with your details include

- Report any issues concerning identity theft to the federal trade commission (FTC)

- Ensure you clean up your entire account

- Immediately contact the credit Report Company and officially place a fraud alert

- In case of Tax-related identity theft, report to the IRS

- Place a block on your credit report

- Contact the company or the backs where the fraud occurred.

LEARN MORE:

KEYWORDS:

- victim

- identity theft

- irs

- fraud

- companies

- account

Answer:

"Organizational schizophrenia" is the appropriate answer.

Explanation:

- It's also provided mostly by examining current literature as well as by adopting a qualitative phenomenological method through conversation as well as interviewing with focused collective discussions.

- That would be a very essential idea to clarify as well as study extensively. There seems to be some consensus among the focal group that perhaps the comparison is quite beneficial for comprehending certain occurrences well within the field of the organization.