Answer: The answer is provided below

Explanation:

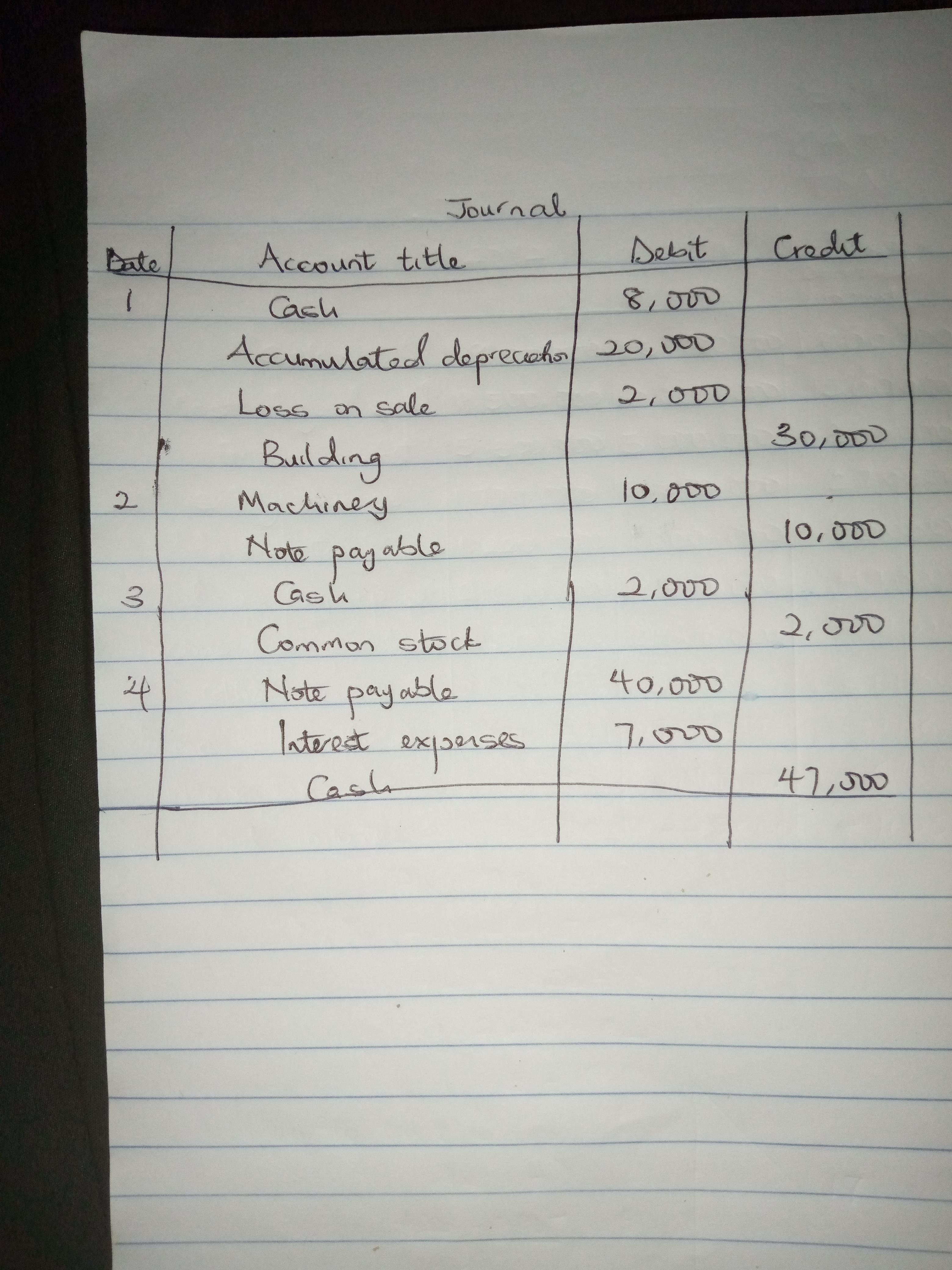

a. The reconstructed journal entry has been prepared and attached.

b. The following are the effects it has on the investing section or the financing section of the statement of cash flows.

The first transaction will lead to a cash inflow of $8,000 from the investing activities.

The second transaction is non-cash transaction therefore, it will not be reported in either the financing or the investing activities.

The third transaction will lead to a cash inflow of $2,000 from the financing activities.

The fourth transaction will lead to a cash outflow from the financing activities.

Thw diagram has been attached.

Answer:

Personalization.

Explanation:

Using personalization in customer relationship management (CRM) requires gathering a lot of information about customers’ preferences and shopping patterns, and some customers get impatient with answering long surveys about their preferences.

This ultimately implies that, personalization deals with gathering information about a specific customer's choice such as taste, requirements, product preferences, shopping styles or patterns in order to be able to serve him or her better, through the provision of goods and services that meets their needs.

The entry to record this event would include a LOSS OF $40,000.

The equipment original cost = $420,000

Accumulated depreciation = $200,000

Selling price = $180,000

Loss = 180,000 - [420,000 - 200,000]

= 180,000 - 220 = - 40,000

Thus, a loss of $40,000 was experienced in the sale of the equipment.

Answer:

(A) unrelated diversification

Explanation:

- The unrelated diversification s a form of diversification that that to the forms of business when they adds up unrelated new products and new lines and penetrates the newer markets.

- An example of cake makers entering a furniture market. Thus relates to different and non-related spheres of functioning.