Nothing really just the header moves where ever you move it to lol

D) sheila is not liable for unauthorized charges made on her card after she reports it stolen.

Also, the last sentence had a grammatical error. --> Past participle without an auxiliary verb.

Answer:

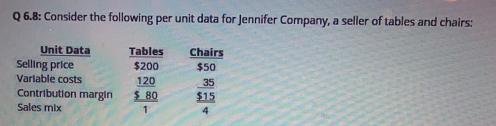

$28 per unit

Explanation:

since the information is missing, I looked for similar questions:

contribution margin per chair = $50 - $35 = $15

contribution margin per table = $200 - $120 = $80

sales mix: 4 chairs + 1 table

contribution margin per sales mix = (4 x $15) + $80 = $140

weighted average contribution margin = $140 / 5 = $28

Answer:

Letter b is correct.<em> A monopolistically competitive firm faces competition from firms producing close substitutes.</em>

Explanation:

<u>Monopolistic competition</u> is an economic situation that occurs when companies exhibit imperfect competition, that is, companies market similar but not identical products, which characterize them as substitute but not perfect substitute products.

Products may have different variables, such as quality, price and reputation in the market. The greater the degree of product differentiation, the more price control the company will have.

A. Hold meetings with employees, volunteers, and representatives of other local shelters and listen carefully as they brainstorm ideas.

C. Honestly acknowledge the challenges the organization faces while also communicating optimism about finding the resources to fulfill your mission.