Question:

The question is incomplete. See the complete question below and the graph.

You are given the following data;

Cost = C = $12,000.00

w = $100.00 per unit of labor

r = $100.00 per unit of capital

These data are used to construct the isocost line (C) in the diagram to the right. Suppose the wage increases to $200.00 but that the firm chooses to keep using the same amount of labor and capital to produce 200 units of output. Given this new set of factor prices (w'=$200.00, r = $100.00), how much have costs changed if the set of input choices remains at point A? Enter a numeric response using a real number rounded to two decimal places.)

Answer:

Cost change = $6,000

Explanation:

Given Data:

Cost = C = $12,000.00

w = $100.00 per unit of labor

r = $100.00 per unit of capital

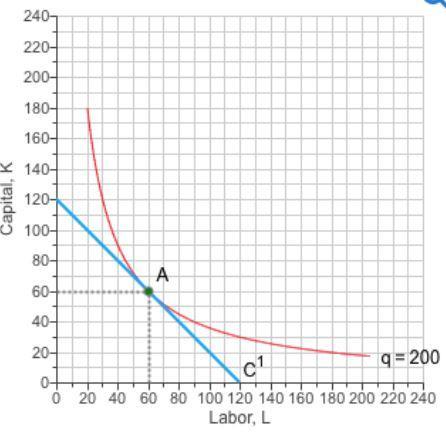

Calculating the cost incurred at point A using the equation of iso-costline C¹, we have;

C = wl + rk

where;

C = total cost

w = price of labor = $100

l = labor = 60 unit from the graph

k = capital = 60 unit from the graph

r = price of capital = $100

Substituting into the formula, we have

C = wl + rk

= 100*60 + 100*60

= 6000+6000

= $12,000

For increase in wages(w= $200, r = $100) with same amount of labor and capital, the cost incurred becomes;

C = wl + rk

= 200*60+100*60

= 12,000 + 6000

= $18,000

Therefore,

Cost change = 18000-12000

= $6,000

See the attached graph.