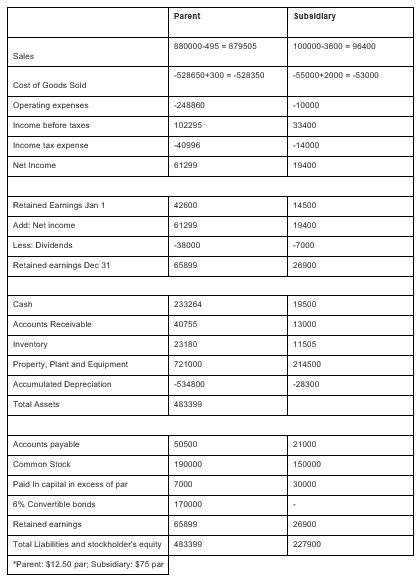

Answer:

Separate financial statement are adjusted and prepared for parents and subsidiaries.

Explanation:

Answer:

Credit cards are neither good nor bad. They are financial tools that must be used with care. Cards can help or hurt your finances if you don't use them responsibly. At the same time, credit cards used properly offer a convenient payment method that can build credit and earn rewards for users.

Explanation:

Answer:

Explanation:

The journal entry to record the bad debt expense is shown below:

Bad debt expense A/c Dr $11,181

To Allowance for doubtful debts $11,181

(Being bad debt expense is recorded)

The computation of the bad debt expense is shown below:

= (Accounts receivable × estimated percentage given

) - (credit balance of Allowance for Doubtful Accounts)

= ($206,300 × 7%) - ($3,260)

= $14,441 - $3,260

= $11,181

Answer:

The correct answer is letter "D": All of the above are true.

Explanation:

The Price-to-Earnings (P/E) ratio represents the relationship between a company's stock share price related to its earnings per share (EPS). The P/E ratio can give investors an idea if a company's share price is undervalued or overvalued. Besides, P/E ratios of companies with similar businesses can be compared to measure firms' performances.

Answer:

Significant noncash financing and investing activities.

Explanation: