Answer: The correct answer is "domination."

Explanation: Our culture has a split personality about big tech companies like Google. On the one hand we are constantly afraid that they are out for world <u>DOMINATION.</u> On the other hand, we love what they offer us and make them our heroes.

Generally, the big global technology companies offer us multiple tools that make it easier for us every day, but on the other hand these companies have a great amount of information from all over the world, with which a lot of damage could be caused if other purposes are pursued.

Answer:

a

Explanation:

with a credit card number that can access you money, name, and your d.o.b

with a d.o.b they cant do anything bc a lot of ppl have the same birthday

phone number they cant do anything bc more than 1 person have the same number like if someones bill wasnt paid, they recycle the #.

place of birth a lot of ppl were born at the same hospital

Answer:

No the suit will not succeed as their is no agreement

Explanation:

The contract was conditional contract. As the condition explicitly said that, the right to agree on terms and conditions is explicitly attorney's right. When the attorney has not agreed on the terms and conditions of Harbor Park, the company hasn't formed any contract. Furthermore, there is no limitation on Grondas to consider other available options and attorney is also not obliged to agree to Harbor's offer.

Thus the suit that says Grondas has breached the contract is meaningless and will not succeed in the court.

Answer:

low-ball technique

Explanation:

Based on the scenario being described it seems that you have been a victim of the low-ball technique. This is a persuasion tactic in which an item is marked at a very tempting low price in order to get customers to commit to the purchase, but when they do commit the price is increased in one way or another. Which in this case was by requiring extra components to be able to use the camera.

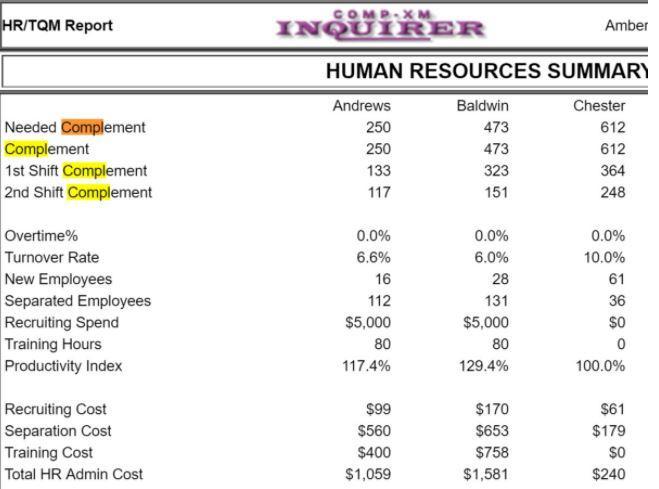

Answer: $362,100

Explanation:

I could not find your exact question's details but I believe this can act as a reference.

Baldwin has 473 employees (given as the Complement). They plan to downsize by 15% which means they plan to retrench;

= 473 * 15%

= 70.95

= 71 people

The cost of retrenching one person is;

= 100 + 5,000

= $5,100

For 71 employees;

= 5,100 * 71

= $362,100