Answer:

- doing online commissions

- Doing house paintings

- Creating a video content online.

Explanation:

- doing online omissions

In this business model Alfonso need to use some sort of website or social medias to promote his skill and services. He need to gathered request from online customers and paint according to their online request

- Doing in house paintings

IN this model, Alfonso will receive house calls from the customers. Alfonso need to come to the customer';s house and draw a portrait of the customers or their family.

- Creating a video content online.

Alfonso could also create online videos about painting tutorial or a follow along video. He can gained profit through ads or sponsors.

Answer and Explanation:

According to the given situation, the income statement and balance sheet as per parts is shown below:-

<u>Accounts Account Title Financial statements </u>

<u>For Part A</u>

Debit Accounts receivable Liability account Balance sheet

Credit Consulting service Income statement

revenue

<u>For Part B</u>

Debit Interest receivable Liability account Balance sheet

Credit Interest revenue Income statement

<u>For Part C</u>

Debit Accounts receivable Assets account Balance sheet

Credit Service Revenue Income statement

<u>For Part D</u>

Debit Janitorial expense Income statement

Credit Janitorial expense Liability account Balance sheet

Payable

<u>For Part E</u>

Debit Rent expenses Income statement

Credit Rent expenses Liability account Balance sheet

payable

Answer:

A. One that decrease taxes and increase spending

Explanation:

No income and more outgoing would create the biggest deficit.

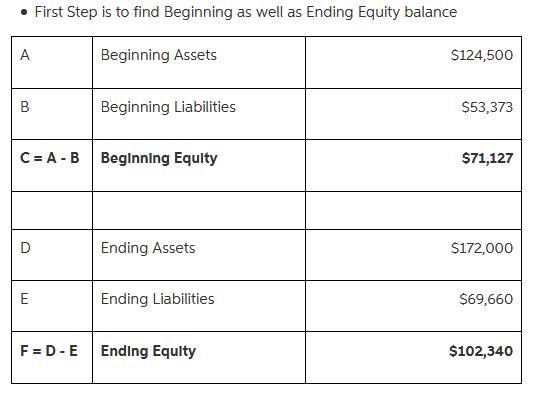

Answer:

Hence, the net income earned or net loss incurred by the business during the year $102,340.

Explanation:

Answer:

The opportunity cost of buying 3 CDs is the lost opportunity to buy 1 DVD

Explanation:

Opportunity cost is the cost of alternative forgone.It is cost of the item not purchased due the current buying decision.

It is also applicable to a business division selling to another division within the company.The cost of such internal sale is viewed as the variable cost of the product plus the contribution forgone from not selling to external party.This is most likely the case when the selling division does not have a spare capacity with which it can fulfill internal sale request.