Opportunity costs are the measures of things you must give up when you make a certain decision.

In this case, if country A decides to produce all petroleum, they are choosing not to produce 8 units of seafood. This is their opportunity costs because they are giving up the 8 units of seafood to make petroleum.

The same is true for country B. If they choose petroleum, they are giving up the ability to make 8 units of seafood.

The saving rate from the highest to the lowest would be :

Traditional Banks +/- 5 % of rates

Online banks +/- 4 % of rates

Credit Union +/- 2.5 % of rates

hope this helps

Answer:

The answer is: A) If taxes are lowered, government revenues actually increase.

Explanation:

For example, when consumers have to pay less money in taxes, it means they will have more money to spend. Private consumption is the most important component of the GDP. When money starts to flow, a virtuous circle of growth starts a chain of events that reinforces economic growth through a feedback loop. When the economic growth rate increases, government revenue will also increase. The virtuous circle of growth is the most important pillar of the Keynesian economic theory.

The same applies to businesses, when they pay less taxes, they can invest more in new businesses which in turn increase economic growth, which results in higher revenue for the government.

Of course this theory applies to certain small tax reductions, and under certain specific circumstances.

Answer:

The answer is: snowball sampling technique

Explanation:

Snowball sampling is used when researchers (or research participants) recruit other participants for a study. Usually it is used when participants are hard to find. The term snowball refers to the idea that once the snowball starts rolling, it will begin to pick up more snow on the way down, increasing in size.

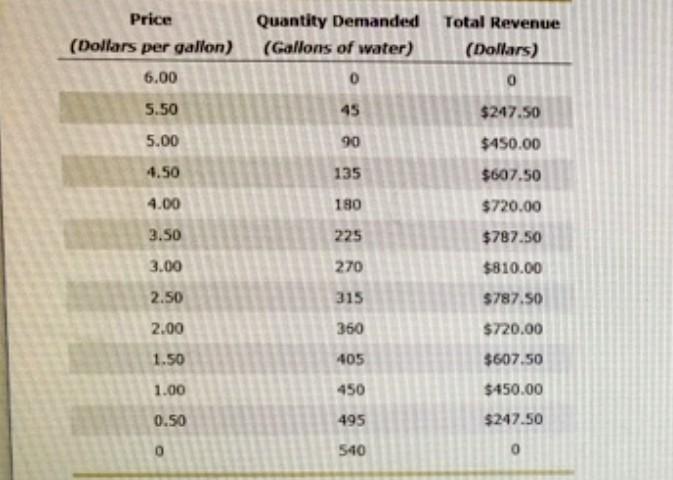

Consider a town in which only two residents, Hubert and Kate, own wells that produce water safe for drinking. Hubert and Kate can pump and sell as much water as they want at no cost. For them, total revenue equals profit.

The following table shows the town's demand schedule for water,

Quantity Demanded Total Revenue (Dollars per gallon) (Gallons of water) (Dollars) $247.50 $450.00 $607.50 4.00 180 $720.00 $787.50 3.00 270 $810.00 $787.50 2.00 $720.00 $607.50 $450.00 $247.50 (Look at attached image for clearer image)

Answer:

$3, $810

Explanation:

By carefully examining the table above we can infer that Hubert and Kate's profit is maximised at $3 unit price.

The total output at this point is 270 with a total Revenue of $810, implying that they will share the amount equally 810/2= $405 for Kate and $405 for Hubert.