Answer:

c. large

Explanation:

If Jill attends a leadership training session at her company’s corporate offices and there are six trainers and 48 participants at the seminar. This would be an example of a <u>large </u>group

By definition large groups are secondary groups of many persons and are impersonal. They are often task-focused and time-limited. They serve an instrumental function rather than an expressive one, implying that their role is more goal- or task-oriented than emotional. Examples include A classroom or office.

Answer:

The correct decision would be to process further before product is sold

Explanation:

Profit if the product is sold un-assembled

Selling price $135

cost of un-assembled product ($60)

Profit on un-assembled product $75

Profit if the product is further assembled before sale

Selling price $170

Cost of un-assembled product ($60)

Cost of assembling product ($25)

Profit if the product is assembled $85

The profit increased by $10 if the product is further assembled before it is sold.

Hence the best course of action would be to further assemble the product before it is sold

Answer:

Supporting them means giving the innovation economy a better chance to find solutions. Startups disrupt, transform and better old ideas and create new ones. By doing so they create new markets and opportunities which in turn create more jobs and improve people's lives.

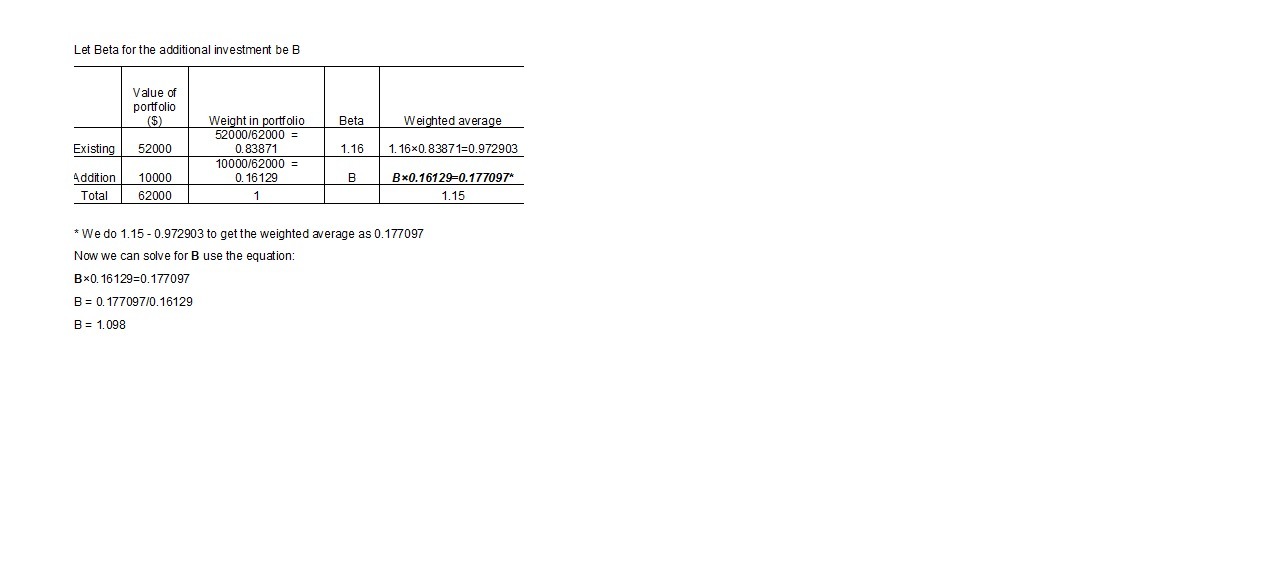

The beta of the new investment must be 1.098.

We need to use the concept of weighted averages to solve this problem.

We find the ratios of the dollar value of existing to the total new portfolio and additional investments to the total new portfolio and find the weights.

We then find the product of the beta of the existing portfolio and its respective weight calculated in the earlier step, with the given data.

We derive the product of the additional investment and beta by subtracting the answer from the earlier step from the new portfolio's beta (1.15).

Then we work backwards to arrive at the the beta for the additional investment.