Answer: D. Select an appropriate transformation process for analysis

Explanation: A flow chart also known as a flow diagram is a schematic representation of how the different stages in a process are interconnected in sequential order. flowchart is a picture of the separate steps of a process in sequential order. It can be adapted for a variety of purposes including manufacturing, administrative, services processes or project plans. The first step in flowcharting is to select the appropriate transformation process for analysis. This involves defining the processes to be diagrammed, discussing and deciding its boundaries or limits: where it would start, where it would end etc. to drawing several major blocks that represent the most important steps in the process.

A.click the chart and ask t edit data

Sing about what you did to get to where you are now, it helps people understand why u starting rapping, many do it to cope with pain. But hey wish you luck!!

Answer:

Explanation:

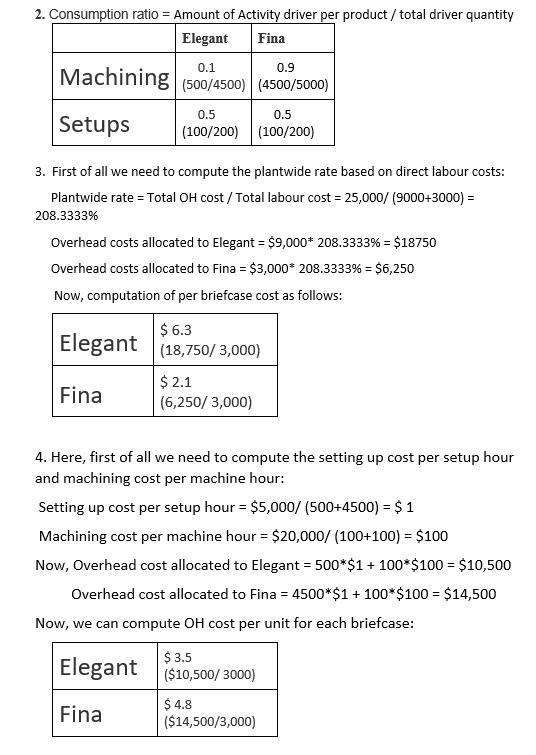

1. Yes, these costs are accurately traced to each briefcase. Because these are variable cost and incurred upon per unit as per the product requirement and specification.

Check attachment for 2, 3 and 4.

For 3b. please provide the statements which are to checked.

Answer:Please refer to the explanation section

Explanation:

The question is incomplete, amounts of production costs like Direct Material, direct labour and Variable/Fixed manufacturing overheard were not given, we will explain the absorption cost and variable cost in detail so that the student would be able to calculate absorption cost and variable cost balances easier.

Absorption costing Method

Total Manufacturing costs are allocated to Finished goods Product. Absorption Costing method assigns or allocates the total cost of Manufacturing or total production costs to units of Finished Goods produced. each unit of finished goods thus represents total costs of production per unit or Total Manufacturing/Production cost is the Balance of Finished Goods.

Total Manufacturing/Production cost = direct labor cost + direct material cost + variable and fixed Manufacturing overheads cost.

Finished Goods Balance = Total Manufacturing/Production cost

A unit of Finished Goods = Total Manufacturing costs/units produced

Variable costing method

Variable costing method fixed manufacturing costs are treated as an expense, Variable Manufacturing costs are the only allocated to inventory. The value or Balance of inventory consist of Variable Manufacturing cost like Direct labor, Direct Material and Variable Manufacturing costs. Finished Goods Balance equals total Variable Manufacturing cost