Answer:

$389,100

Explanation:

Calculation to determine what the correct balance for ending inventory on December 31 is:

Using this formula

Ending inventory on December 31=Ending inventory balance-Office supplies

Let plug in the formula

Ending inventory on December 31=$414,500- $25,400

Ending inventory on December 31=$389,100

Therefore the correct balance for ending inventory on December 31 is:$389,100

Answer:

4.93%

Explanation:

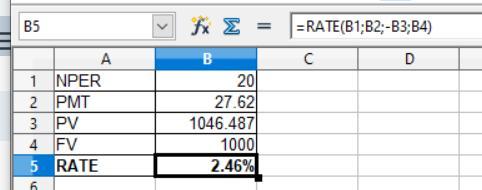

For computing the yield to maturity we need to apply the RATE formula i.e to be shown in the attachment below:

Provided that,

Present value = $1,046.487

Future value or Face value = $1,000

PMT = 1,000 × 5.524% ÷ 2 = $27.62

NPER = 10 years × 2 = 20 years

The 10 years is come from

= May 2029 - May 2019

= 10 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after applying the above formula,

The yield to maturity is

= 2.46% × 2

= 4.93%

Answer:

According to Bernstein, higher level professionals are strategic thinkers, while those at the lower levels are more tactical thinkers. More advanced individuals understand the big picture of where the organization is going and how all the different parts are interconnected.

Explanation:

Answer:

A. $250,800

B. $150,000

Explanation:

a. Calculation for maximum price

First step is to find the Earnings per year amount using this formula

Earnings per year= ROI×Plant and equipment replacement value

Let plug in the formula

Earnings per year=198,000*19%

Earnings per year=37,620

Second step is to calculate for the maximum price using this formula

Maximum price=Earnings per year/ROI

Let plug in the formula

Maximum price=37,620/15%

Maximum price= 250,800

Therefore maximum price is $250,800

b. Based on the information given each of the asset that each individual acquired will be recorded at the market fair value amount while the amount of $150,000 will be recorded as Goodwill.

Using this formula to calculate Goodwill amount

Goodwill =Purchased amount- Fair value

Let plug in the formula

Goodwill=750,000-600,000

Goodwill=$150,000

Consider a good that generates external damages. A competitive market that is left un-regulated tends to. charge a lower price than the price that would result in maximized social welfare.

A market is a composition of structures, establishments, approaches, social members of the family or infrastructures wherein events interact in alternate. whilst parties may alternate goods and services by barter, maximum markets rely on sellers imparting their goods or services to consumers in alternate for cash.

A market is described as the sum general of all the consumers and sellers in the location or region under consideration. The area may be the earth, or international locations, regions, states, or cities. The cost, cost and rate of items traded are as in step with forces of deliver and demand in a market.

Learn more about market here:brainly.com/question/906651

#SPJ4