The answer is B. A system that regulate by the interactions between producers and consumers

I hope this help and can u plz give me brainlist

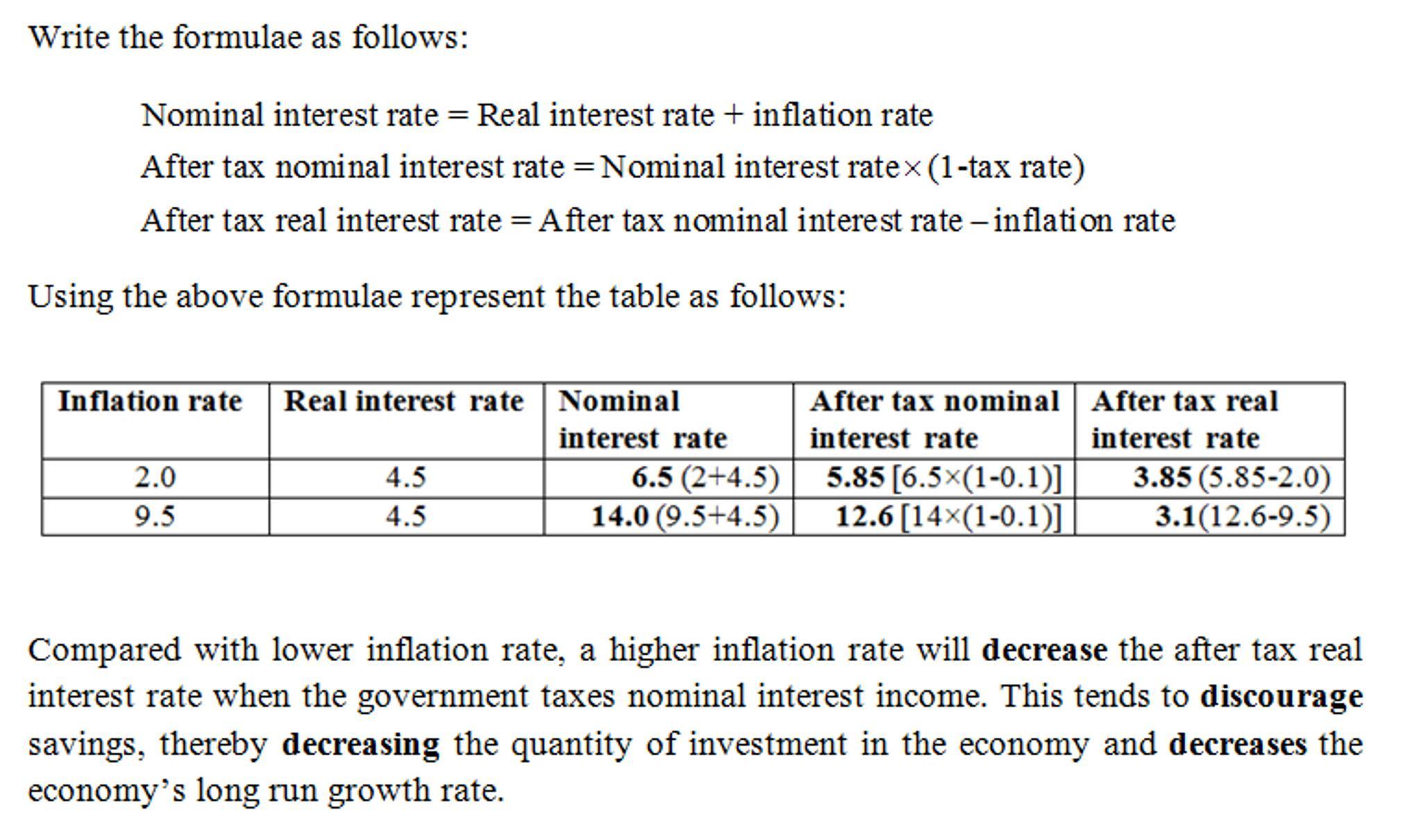

Answer

The answer and procedures of the exercise are attached in the following archives.

Explanation

You will find the procedures, formulas or necessary explanations in the archive attached below. If you have any question ask and I will aclare your doubts kindly.

Service advantage is like the four noble truths of Buddha, Dukka, Samudaya,Nirodha and Magga. It explains, How it works in life and how it works in business opportunity it is interrelated Dukka is suffering, Samudaya is cause of suffering, Nirodha is end to suffering , Magga is path to suffering which can correlate to Empathize, Analyse, Solve and Test example Amazon anything from AtoZ at your door step.SWOT analysis is the big four in finding your pros and cons of business. It lets your compare with your marks and extra curricular activity with colleagues it helps you the amount of work you can complete with your colleague. Example your are at school your marks is average as per your SWOT analysis you will work in a average company,At work if you work for MIS(Management information system) if your colleague is advance in excel he would be picked maximum number of time then you. SWOT lets you solve those criteria s.

Explanation:

- Dukka suffering, Empathize human services issues.

- Samudaya root cause of suffering, Analyze data on requirement.

- Nirodha end of suffering, Solve an advent finding a solution.

- Magga path to suffering, Test reworking it and finding your SWOT.

- SWOT place a major role in Marketing and as a personality.

- Always know all the four objects of SWOT.

- Apple company worked it out very well with SWOT.

- Lego came up with multidimensional business.

- Nokia failed to interpret SWOT and always believed they were better.

Answer:

Higher prices

Explanation:

Fixed prices are associated with higher prices for consumers

Answer:

Letter b is correct. <u>Time frame.</u>

Explanation:

The SMART system is defined as an aid tool for achieving goals. It is a tool that can be used both by an individual and in corporations.

In order to achieve a goal, it is necessary to have the ideal planning of the set of actions that will contribute to the achievement.

Therefore, each letter of the word SMART corresponds to a meaning relevant to the effective implementation and achievement of a goal

S: specific. When drawing up a goal you must be direct and specific.

M: Measurable. To achieve goals, it is necessary to use a tangible indicator that assists the measurement.

A: Achievable. A goal must be planned according to the real possibility of being achieved.

R: Relevant. Goals must be relevant and create positive results for a person or organization.

T: Time. It is necessary to determine a time for the goal to be achieved. In the question above, Amy lacked the planning for the deadline for achieving the goal, because without it there are great chances that the goal will not be taken seriously and not met.