Answer:

Dr Merchandise inventory 50,000

Dr Machinery 155,000

Dr Notes receivable 100,000

Cr Common stock 62,000

Cr Additional paid in capital in excess of par value 243,000

Explanation:

All outstanding stocks must be recorded at par value: 3,100 shares x $20 = $62,000. Any mount paid for the stocks in excess of par value must be recorded in the additional paid in capital in excess of par value account : $305,000 - $62,000 = $243,000

<span>Your debt to income ratio determines how likely you are able to make your payments. When a high percentage of your available credit is been used, this can indicate that your money is overextended, and you may be more likely to make late and or missed payments.</span>

Answer:

$14,832

Explanation:

Depreciation charge = 2 x SLDP x BVSLDP

where,

SLDP = 100 ÷ useful life = 20 %

and

BVSLDP = Cost or Net Book Value

therefore,

1st year

Depreciation charge = 2 x 20 % x $61,800 = $24,720

2nd year

Depreciation charge = 2 x 20 % x ($61,800 - $24,720) = $14,832

conclusion

the amount of depreciation for the second full year is $14,832

C.

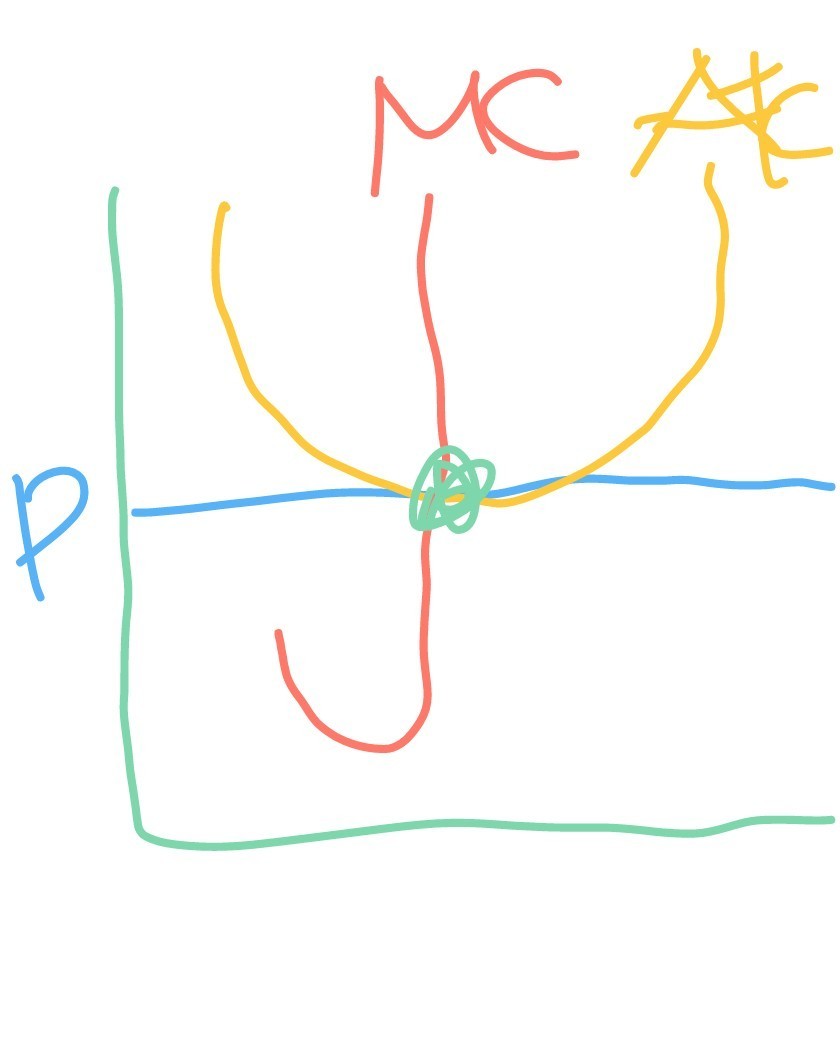

Allocative efficiency in simple terms basically means there is no wastage, therefore if producers produce at price equals marginal coat, they are producing at the point where consumers are willing to pay that final price. Refer to the poorly drawn diagram for reference.

Answer:

Net income= $2,328,000

ROA= 12%

ROE= 25.30%

Explanation:

Aquilera incorporation has a sales of $19.4 million

The total assets is $14.4 million

The total debt is $5.2 million

The profit margin is 12%

The net income can be calculated as follows

= profit margin × sales

= 12/100 × 19,400,000

= 0.12 × 19,400,000

= $2,328,000

The ROA can be calculated as follows

= Net income/Average Sales

= 2,328,000/19,400,000

= 0.12 × 100

= 12%

The ROE can be calculated as follows

= Net income/Total equity

Total equity= Total assets - Total debt

= 14,400,000-5,200,000

= 9,200,000

= 2,328,000/9,200,000

= 0.2530 × 100

= 25.30%