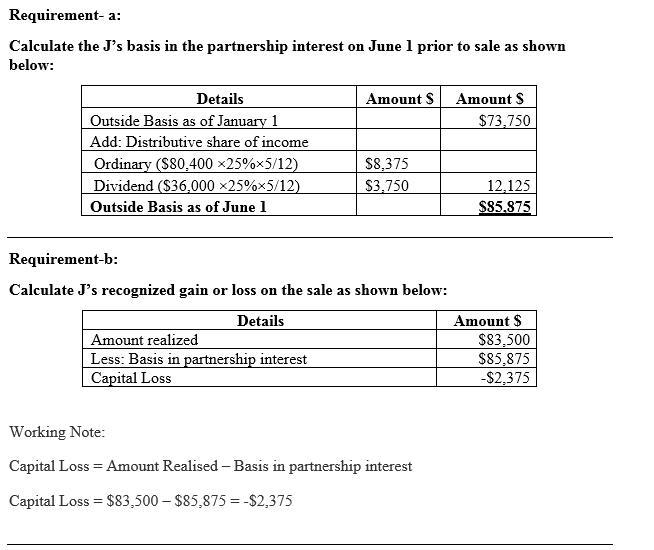

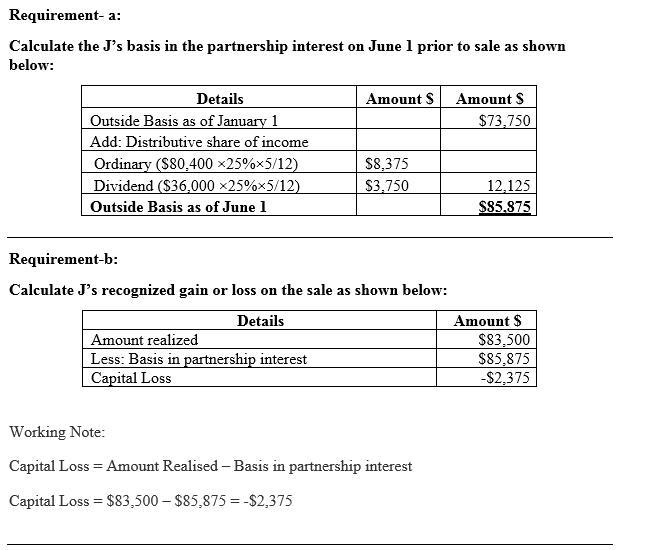

ry 1 of the current year, James’s basis in his partnership interest is $73,750. For the taxable year, the partnership generates $80,400 of ordinary income and $36,000 of dividend income. For the first five months of the year, GJHC generates $25,750 of ordinary income and no dividend income. On June 1, James sells his partnership interest to Robert for a cash payment of $83,500. The partnership has the following assets and no liabilities at the sale date: (Do not round your intermediate calculations. Round your final calculation to the nearest whole dollar amount. Enter a loss as a negative number.)

Tax Basis FMV

Cash $ 38,500 $ 38,500

Land held for investment 83,500 108,200

Totals $ 122,000 $ 146,700

a.

Assuming GJHC’s operating agreement provides that the proration method will be used to allocate income or loss when p

artners’ interests change during the year, what is James’s basis in his partnership interest on June 1 just prior to the sale?