Answer:

Asset Price= $746,617.36

Explanation:

Giving the following information:

Face value= $1,000,000

Coupon= 0.03/2= 0.015*1,000,000= $15,000

Number of periods= 2*4= 8 semesters

YTM= 0.11/2= 0.055

<u>To calculate the price of the asset, we need to use the following formula:</u>

<u></u>

Asset Price= cupon*{[1 - (1+i)^-n] / i} + [face value/(1+i)^n]

Asset Price= 15,000*{[1 - (1.055^-8) / 0.055} + [1,000,000 / (1.055^8)]

Asset Price= 95,018.49 + 651,598.87

Asset Price= $746,617.36

Answer:

(1) $1,885

(2) $1,540

Explanation:

Given the following sequence:

200 units at $5, 600 units at $6 and 145 units at $7

Ending inventory = 290 units

(1) FIFO method

Cost of ending Inventory:

= 145 units at $7 + 145 units at $6

= 145 × $7 + 145 × $6

= 1,015 + 870

= $1,885

(2) LIFO method

Cost of ending Inventory:

= 200 units at $5 + 90 units at $6

= 200 × $5 + 90 × $6

= 1,000 + 540

= $1,540

There is a good chance that no one would buy anything cause of the high prices...

D. Increased personal workload

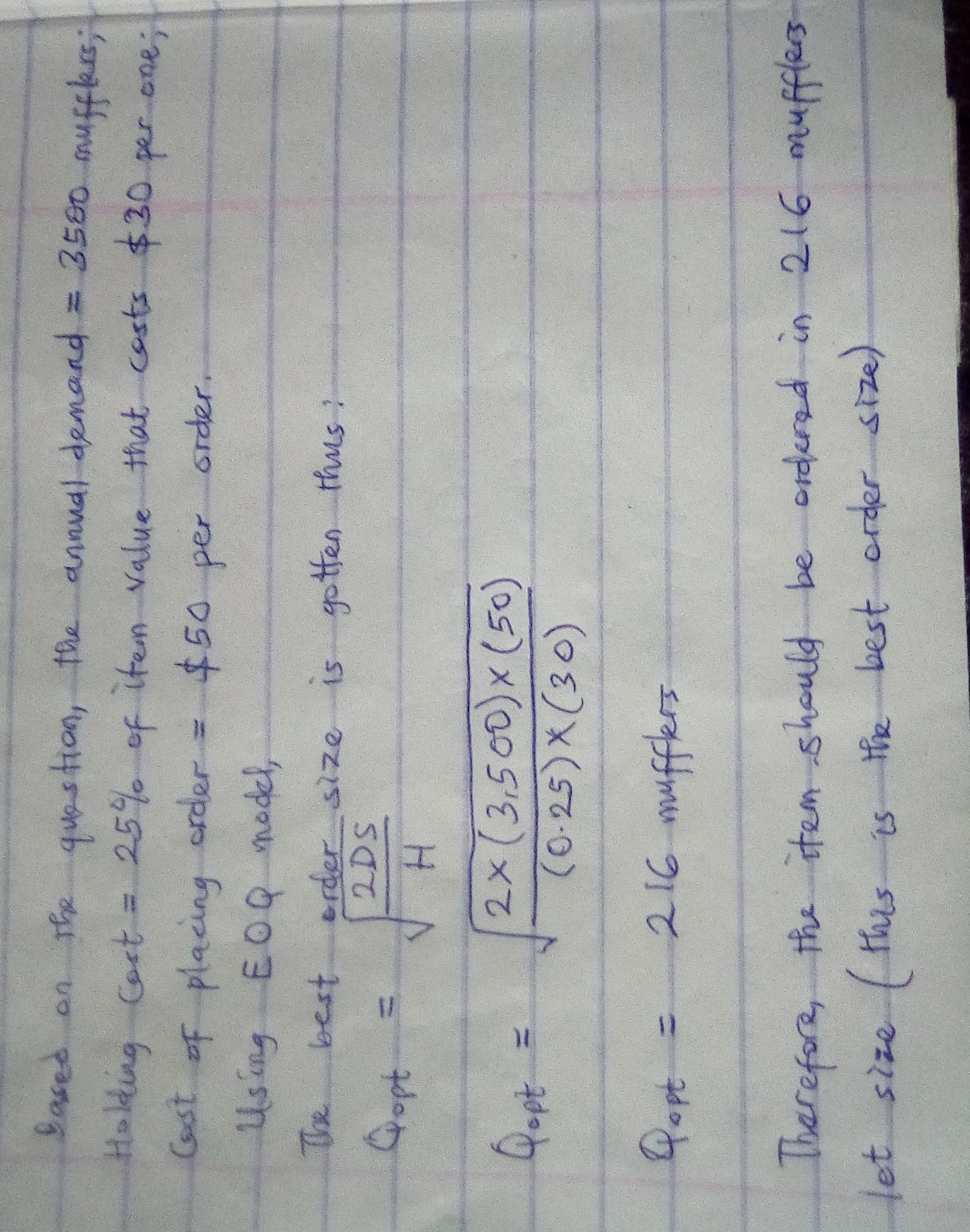

COMPLETE QUESTION:

Sarah’s Muffler Shop has one standard muffler that fits a large variety of cars. Sarah wishes to establish a reorder point system to manage inventory of this standard muffler. Use the following information to determine the best order size:

(The attachment contains the information)

Answer: 216 mufflers is the best order size.

Explanation:

The attachment contains the calculations and information.