Answer:

the part where you have to lead

Explanation:

Answer:

See attached file

Explanation:

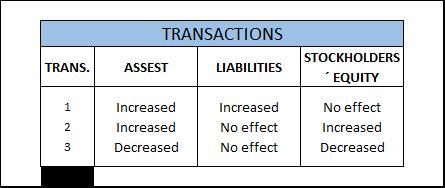

Accounting Equation Formula:

Assets = Liabilities + Stockholders' Equity

The equation shows that Assets are increased by Debits and decreased by Credits, instead, Liabilities and Stockholders´ Equity decreased by Debits and increased by Credits. In the file, Debits and Credits are represented by the word increased and decreased according to if the transaction has a positive or negative effect on each element.

Answer:

The correct answer is B.

Explanation:

Giving the following information:

Unit sales 50,000

Units Dollar sales $ 500,000

Fixed costs $ 204,000

Variable costs $ 187,500

First, we need to calculate the unitary selling price and variable cost:

Unitary Selling price= 500,000/50,000= $10

Unitary variable cost= 187,500/50,000= $3.75

Break-even point (dollars)= fixed costs/ contribution margin ratio

Break-even point (dollars)= 204,000/ [(10 - 3.75)/10]= $326,400

18.9%

Finding a company's cost of capital is crucial in corporate finance for a few key reasons. For illustration, a corporation might calculate its net present value using the WACC discount rate. A lower WACC typically denotes a healthy company that can draw investors at a reduced cost. The industry has three firms with un levered betas of 0.7, 1.1, and 1.6. the discount rate to use for a un levered firm that wants to enter this industry is 18.9% if the risk-free rate is 3 percent and the expected return on the market is 17 percent

The WACC discount formula is: WACC = E/V x Ce + D/V x Cd x (1-T)

To learn more about WACC please refer to -brainly.com/question/14223809

#SPJ4

Answer: 2.0 and 16%

Explanation:

The degree of operating leverage and the expected percent change in income, will be calculated thus:

Operating leverage will be:

= Contribution margin / Net operating income

= 49200 / 24600

= 2

Then, percentage change in income will be:

= %change in sale × operating leverage

= 8% × 2

= 16%