The statement above is TRUE.

In common law countries, ownership of an intellectual property is established by prior use while in code law countries ownership is established by the registration of that property. Which means that legal ownership in one country does not necessarily mean ownership in other countries.

Answer:

If the salt concentration in the cup is higher than inside the potato cells, water moves out of the potato into the cup.

Explanation:

How his decision will affect the rights of his employees, his consumers, and others

Answer:

$211,971.

Explanation:

he will have earned in $115,971 in interest.

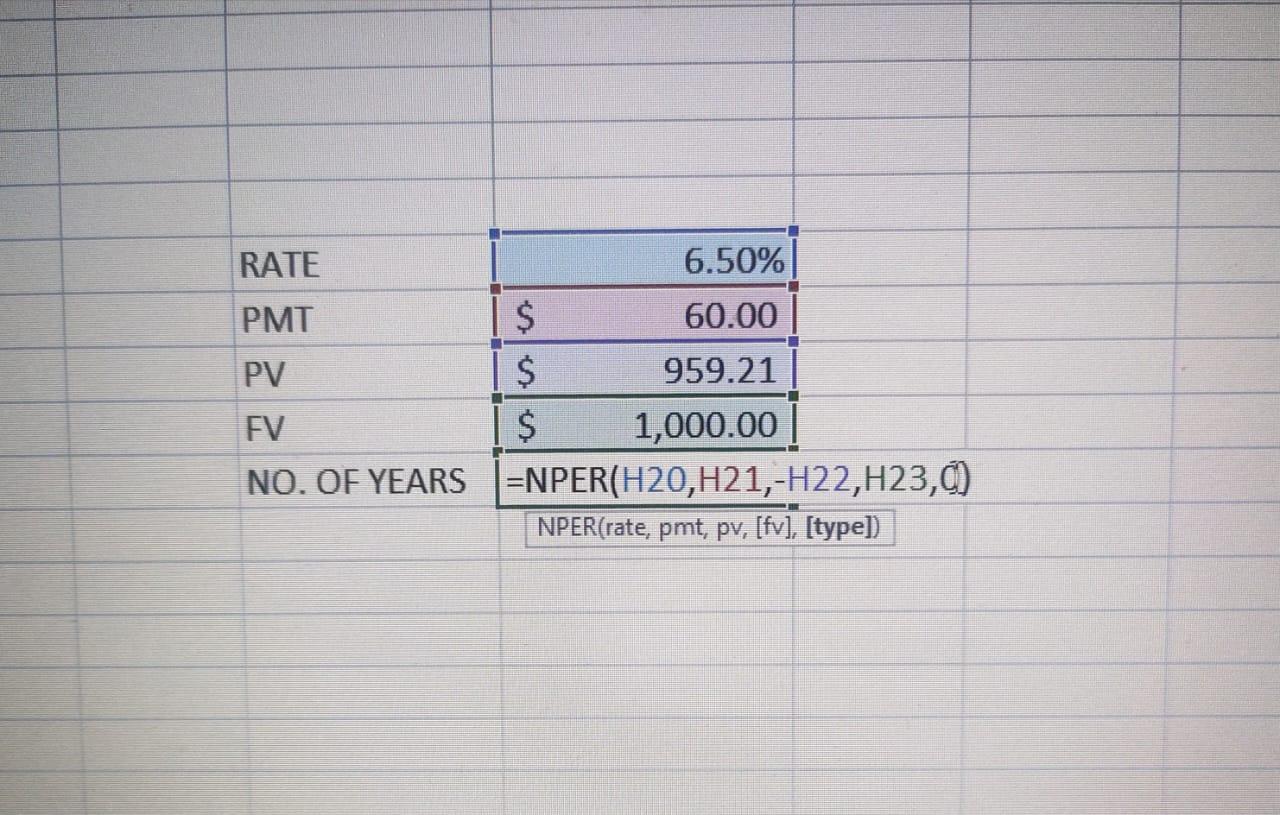

At the current interest rate of 6.5%, the bonds will mature in 12 years.

CALCULATIONS:

RATE= 6.5%

PMT= 1000$*6% = 60$

PV= 959.21$

FV= 1000$

NO. OF YEARS TO MATURE= NPER(rate, pmt, -pv,fv,0)

=NPER(6.5%,60$,-959.21$,1000$,0)

=12 YEARS

A coupon bond, also known as a bearer bond or bond coupon, is a debt obligation that includes semiannual interest coupons. The issuer keeps no record of coupon bond purchasers, and the purchaser's name is not printed on any kind of certificate. Between the time the bond is issued and the time it matures, bondholders receive these coupons.

Coupons are typically described in terms of the coupon rate, which is the yield paid on the date of issuance by a coupon bond. The interest rate on the coupon is subject to change. The coupon rate is calculated by adding all of the annual coupons and dividing the total by the bond's face value.

Learn more about coupon bonds here:

brainly.com/question/14746407

#SPJ4