Size of the organization, business model, nature of business and location are key factors in determining an organization's structure.

They were fighting the russians and lost.

Answer:

C.

Explanation:

Financial Statements depicts the financial position of a firm at a particular point of time or specified date. The users of financial statements use various types of analysis to understand or compare the current financial statements of the company to prior years or with those of the competitors.

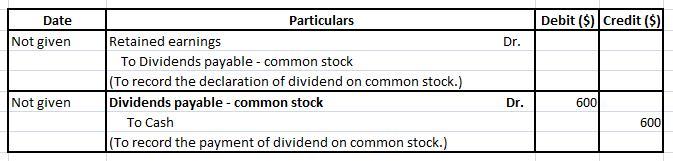

The journal entry on declaration of dividend would lead to a debit to retained earnings and credit to dividends payable.

No journal entry is passed on the date of recording dividend.

Later, on the date of payment of dividend would lead to a debit to dividends payable and credit to cash account.

The journal entries have been shown below:

Networking is a socioeconomic business activity by which business people and entrepreneurs meet to form business relationships and to recognize, create, or act upon business opportunities, share information and seek potential partners for ventures.