Answer:

shift demand and supply for loanable funds to the right (up), increasing interest rates.

Explanation:

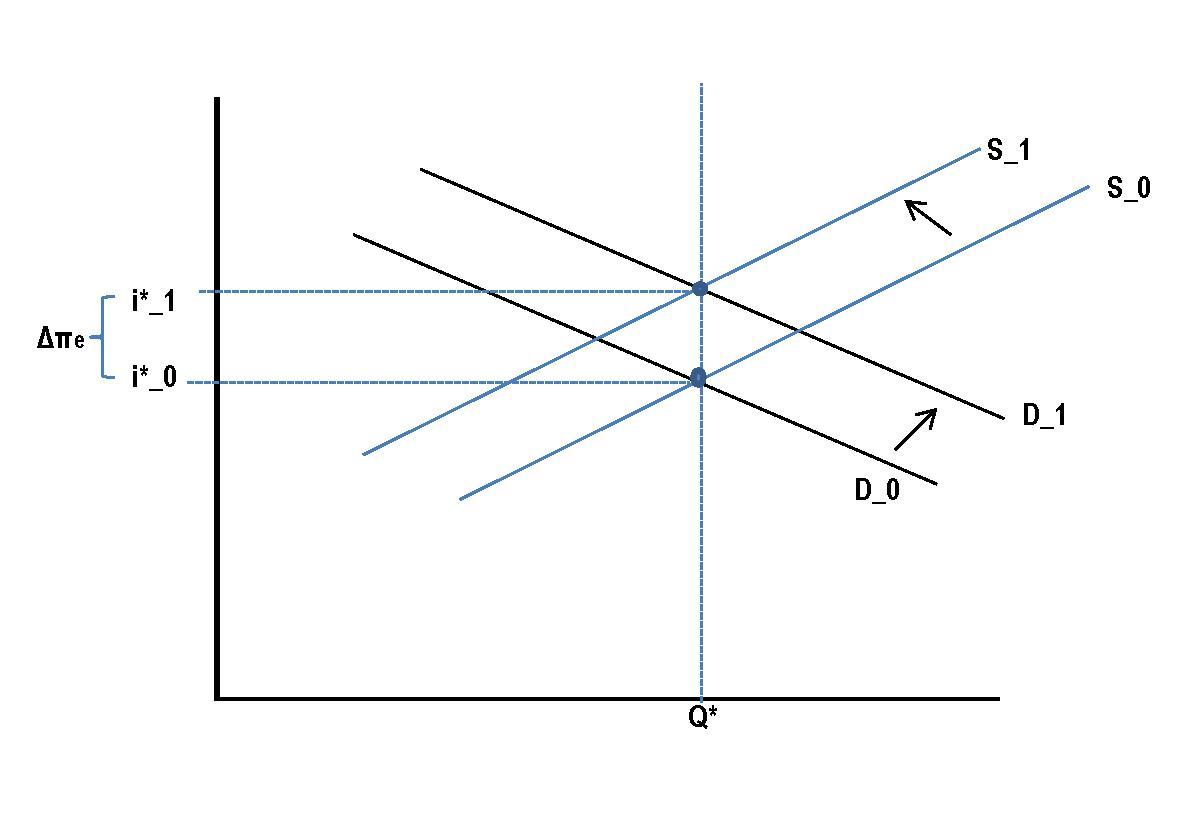

According to the Fisher hypothesis when there is an increase in the expected inflation there is an equal increase in nominal interest rates.

As interest rates rise demand and supply for loanable funds will rise. This is illustrated in the attached diagram. Interest rate moves from i0 to i1.

Inflation is a reduction in the purchasing power of money. When inflation increases money regulation agencies reduce supply of money as a way to reduce price increase. This in turn reduces the amount of loanable funds commercial banks have to give out

Please answer please please thank you so please answer answer

Joint venture is when two companies ask to do part or full of their job.