<span>a similar position in the same company with the same pay as their old jobs.</span>

Answer:

I would buy the 2000 Toyota Tundra. Yes it is the most expensive, but it is the newest so it should require less expense money for problems, it is a manual transmission 6 cylinder so it should get better gas mileage, and it has fewer miles. The rankings of these trucks are not provided, however a Toyota tundra is considered to be a workhorse in the truck. If this is an opinion question, that's my choice.

Explanation:

Answer:

the interest expense that should be recorded in the income statement is $600

Explanation:

The computation of the interest expense is shown below:

= Borrowed amount × rate of interest × given months

= $60,000 × 0.03 ÷ 12 × 4 months

= $600

Hence, the interest expense that should be recorded in the income statement is $600

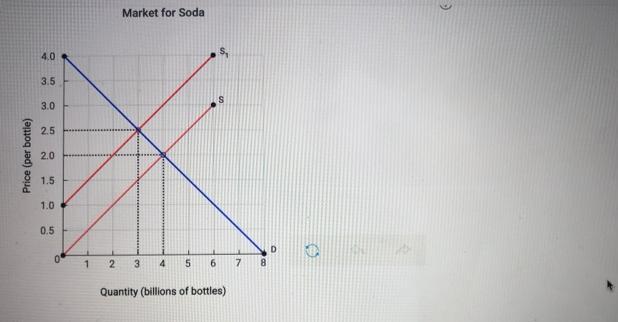

Answer: hello your question is poorly structured attached below is the missing graph and missing part of the question

Assume the government imposes a $1.00 excise tax on the sale of every 2 liter bottle of soda. The tax is to be paid by the producers of soda. The figure below shows the annual market for 2 liter bottles of soda before and after the tax is imposed.

answer :

a) $2 , 4 billion

b) $2.5

c) $1.5

d) 3 billion

e) $3 billion

Explanation:

a) equilibrium price = $2 per bottle

equilibrium quantity = 4 billion bottles

<u>b) After imposition of excise tax </u>

consumers will pay = $2.5

<u>c) The amount producers keep after the imposition of taxes </u>

= $2.5 - tax

= 2.5 - 1 = $1.5

<u>d) New equilibrium quantity ( after tax is imposed ) </u>

= 3 billion bottles ( from graph attached ) i.e. intersection of S2 and D

e)<u> Amount of tax revenue collected by the government from the imposition of tax </u>

= quantity of bottles sold * $1

= 3 billion * $1 = $3 billion

The people who may be significantly affected by the outcome of this negotiation by the manager include the employer and the customers.

<h3>Who is a manager?</h3>

It should be noted that a manager simply means an individual who oversees the team in a company and ensures that the goals of the company are achieved.

In this case, Ken is the produce manager at saying way a large Supermarket that is part of a national chain and after completing a few management courses offered by his employer, as well as five years of service at the supermarket, he is up for a promotion to assistant manager and is about to negotiate his new salary.

In this case, the people who may be significantly affected by the outcome of this negotiation by the manager include the employer and the customers. This was illustrated in the information.

Learn more about manager on:

brainly.com/question/24553900

#SPJ1