In order to determine whether to major in economics, a rational individual compares the <u>marginal benefit </u><u>and</u><u> marginal cost.</u>

<u></u>

Marginal benefit is the maximum amount a consumer is willing to pay for additional goods or services. Consumer satisfaction tends to decline as consumption increases. Marginal cost is the change in cost when additional units of a good or service are produced.

Marginal utility and marginal cost are related in many ways in manufacturing and production, investment, and consumption. Marginal cost (MC) is the cost of the last unit produced or consumed, and marginal utility is the utility gained from that last unit.

Marginal benefit is the increase in total utility due to a unit change in the output of a good. Marginal cost is the increase in total cost caused by a one-unit change in the output of a good.

Learn more about the marginal benefit and marginal cost

brainly.com/question/21060213

#SPJ4

Answer:

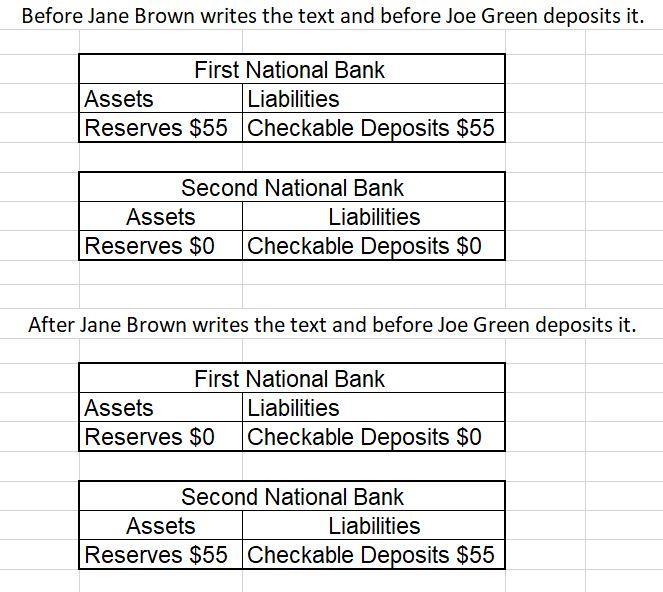

Please refer to the attached.

Before Jane Brown wrote the check, her account was $55 at First National Bank which is reflected by the checkable deposit of $55 which the bank will keep in reserve as an asset.

Joe Green has not received the money so his account at Second National will show $0 balances.

After the cheque has been written and deposited, Jane Brown's chekcable deposits at First national will become $0 as well as the reserves.

Joe Green on the other hand, having gained the $55 and deposited it will see his checkable deposits rise to $55 which the bank will keep in reserve as an asset.

Answer:

1. How is a bond like an IOU?

A bond is an IOU because it is actually a type of IOU. A bond is in essence a security in which the bond issuer promises to pay the bondholder the full value of the bond at maturity, plus interest payments (coupons) that can be paid either periodically, or at maturity as well.

2. Why is an investment grade bond is considered a “safe” investment?

Investment grade bonds are those bonds that have a rating that is considered "safe". This rating is provided by agencies such as Standard and Poors or Moody's. It is the credibility behind these agencies that makes a bond with that type of rating a safe investment.

3. How can an investor make money by buying a bond?

The investor makes money because he or she obtains the full value of the bond at maturity plus interest (coupon payments).

Bondholders also have priority over stockholders in case of bankruptcy, so a bond is in many cases a safer investment than a stock.

4. Would you recommend your Stock Market Game team include a bond in your portfolio? Why, why not?

Yes, bonds should be included because they are one of the two main types of securities, the other being stocks precisely. Companies often have to take the decision to finance their operations either with bonds or stocks, or a combination of the two, so if the game includes bonds, it also becomes more realistic.

Answer:

A) At point C, 2 automobiles will equal 9 forklifts. Therefore, an extra automobile would cost 4 and a half forklifts.

B) Also, because 6 forklifts equal 2 automobiles, an additional forklift would cost 1/3 automobiles

Explanation:

It only costs 3 forklifts to manufacture the first two cars; the next pair comes at a cost of 6 forklifts. Therefore, it will cost a dozen forklifts to manufacture the last 2 automobiles. This demonstrates that every extra car produced comes at a greater cost than the one before.

Cheers

Answer:

Implied agency

Explanation:

Agency

This is simply known as a form of

relationship between two parties in that the principal hires another person to represent him or her.

An agency relationship can be created with 2 types of agreements between the parties. They are

1. Express agency

2. Implied agency

Express agency

This is simply known as a formal contractural agreement. It can be in an oral or written format.

Implied agency

This is often regarded as an implied agreement. It is an agency which is created through the actions of the parties, instead of an express agreement. It is also called Ostensible agency.

Listing Agreement

This is simply defined as written employment contract which gives right to the broker to find a buyer or a tenant for the owner's property.