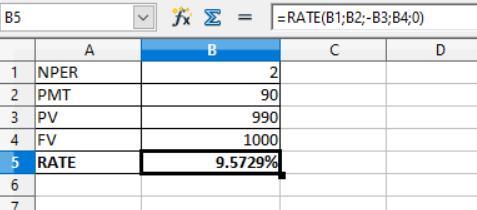

Answer:

the annual required rate of return is 9.57%

Explanation:

The computation of the required rate of return is shown below:

Given that

Future value = $1,000

Present value = $990

PMT = $1,000 × 9% = $90

NPER = 2

The formula is shown below:

=RATE(NPER;PMT;-PV;FV;TYPE)

The present value comes in negative

After applying the above formula, the annual required rate of return is 9.57%

Answer: 1.6 cheesecakes

Explanation: Opportunity cost is simply the cost of a forgone alternative. It is the cost of an opportunity forgone (and the loss of the benefits that could be received from that opportunity); the most valuable forgone alternative.

If Marv can decorate 8 wedding cakes or 13 cheesecakes, it follows that the opportunity cost of making 8 wedding cakes is 13 cheesecakes. The question asks the cost of making a cake. This is given by:

13/8 = 1.625 cheesecakes

= 1.6 cheesecakes to the nearest tenth as the answer.

Tabor company issues $20,000 of common stock to investors. recording this transaction will include a credit to common stock. A security that symbolizes ownership in a firm is called common stock. After creditors, bondholders, and preferred stockholders have been paid, whatever assets are left over after a liquidation go to common stockholders.

In the firm, various kinds of equities are traded. In other words, it's a method of allocating corporate ownership; as a result, each share of common stock corresponds to a certain proportion of a corporation. One share, for instance, would represent one percent ownership of a firm with 100 outstanding shares.

To learn more about common stock, click here.

brainly.com/question/9970004

#SPJ4

Answer:

Revenue should be recognized in the period goods and services are provided.

Explanation:

IFRS 15 requires revenue to be recognized when control of goods or services has been made to the customer. Control is when all the risks and benefits associated with the product or service has been transferred to the customer.

Answer:

most circumstances

Explanation:

The priority in the interests those that have companies to present them first or those that have perfected it. This is due to giving it greater agility on the side of presenting it first and having the interests very explicit as soon as possible and on the other hand when they have been perfected giving greater integrity to the interest presented by the company.