Answer:

The right answer is B.

Explanation:

The equation is glucose + oxygen ==> carbon dioxide + water and energy is produced in the form of ATP.

Cellular respiration is a complete breakdown of glucose in the presence of oxygen, allowing a total release of its energy.

Glucose is "burned" in the presence of oxygen in the cells of animals and plants.

Breathing releases energy stored in glucose (during photosynthesis). The majority of this energy is transferred to ATP which can be used by all cells.

And the waste of respiration is carbon dioxide and water, which are precisely the raw materials of photosynthesis in chloroplasts (= closed circuit).

Answer:

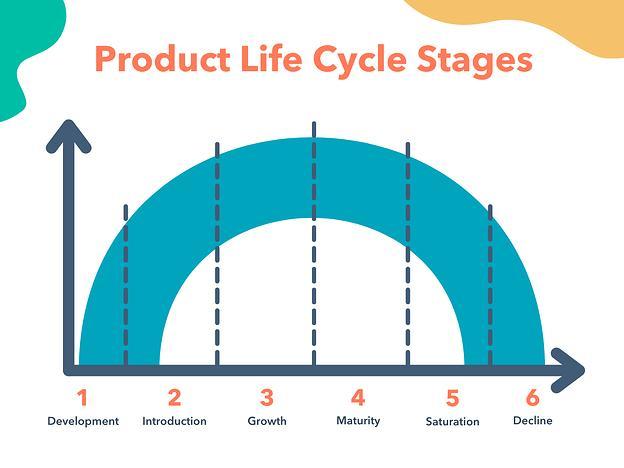

Depending on how many stages you like to go by here are the phases

<u>6 Stages:</u>

1. Development

2. Introduction

3. Growth

4. Maturity

5. Saturation

6. Decline

<u>4 Stages:</u>

1. Development/Introduction

2. Growth

3. Maturity

4. Decline

Explanation:

Check the Attached Image!

Answer:

The increase in operating profit is $1,829.00.

Explanation:

The rise or fall in the operating income:

= Purchase unit × ( offer price- direct material- direct labor- variable overhead)

The rise or fall in the operating income: = 1550× (2 - 0.26 - 0.4 - 0.16)

The rise or fall in the operating income: = $1829

Therefore the profit will increase by $1829

Here all the fixed cost is not considered because it is a sunk cost and variable and administrative expenses are also not considered because these costs are not going to be incurred for offer.

Answer:

<h2>

W Smith, a sole trader</h2>

Identification and Explanation of Highlighted Accounting Concepts and Treatment in the Final Accounts:

1. Economic Entity: The business (economic entity) is separate from the individual (W. Smith). Accounts are kept to ensure this separation of ownership from the business. This withdrawal is treated as Drawings, a reduction of capital (owner's equity) in the balance Sheet.

2. Consistency concept: This concept requires that an accounting estimate or principle is consistently applied. However, if there is a change in an accounting estimate, the effect of the change needs to be disclosed in the final accounts.

3. Going concern concept: A business is assumed to continue indefinitely in life. Therefore, assets and liabilities are stated at their cost or fair values. Where there is a contrary view, this must be disclosed and accounts be kept to reflect the revised view. Then, assets and liabilities will reflect market or disposal values.

4. Materiality concept: This concept requires that values in accounts be material. Though, materiality is a matter of judgement, a threshold can be established based on the value of the individual item to the value of the business. Will its disclosure or not affect decisions of a knowledgeable investor or analyst, is a consideration under the materiality concept. The office stationery can be expensed in the income statement if the amount involved is not material, even though, they will continue to be used in the business for more than a year. This somehow contradicts the concept of the matching principle.

5. Accrual Concept: The concept states that "Revenue is recognized when earned, and expenses are recognized when assets are consumed," and not when cash is received or paid. This unpaid electricity bill for £900 must be accrued in the income statement as an expense and treated as a liability in the balance sheet in line with the accrual concept.

Explanation:

These are the basic accounting concepts:

1. Accruals concept

2. Conservatism concept

3. Consistency concept

4. Economic entity concept

5. Going concern concept

6. Matching concept

7. Materiality concept

Answer:

There are different factors that play into the costs.

Explanation:

For example, if you are a male, you tend to be more reckless. It also depends on the job you would be working at.