Answer: Check attachment

Explanation:

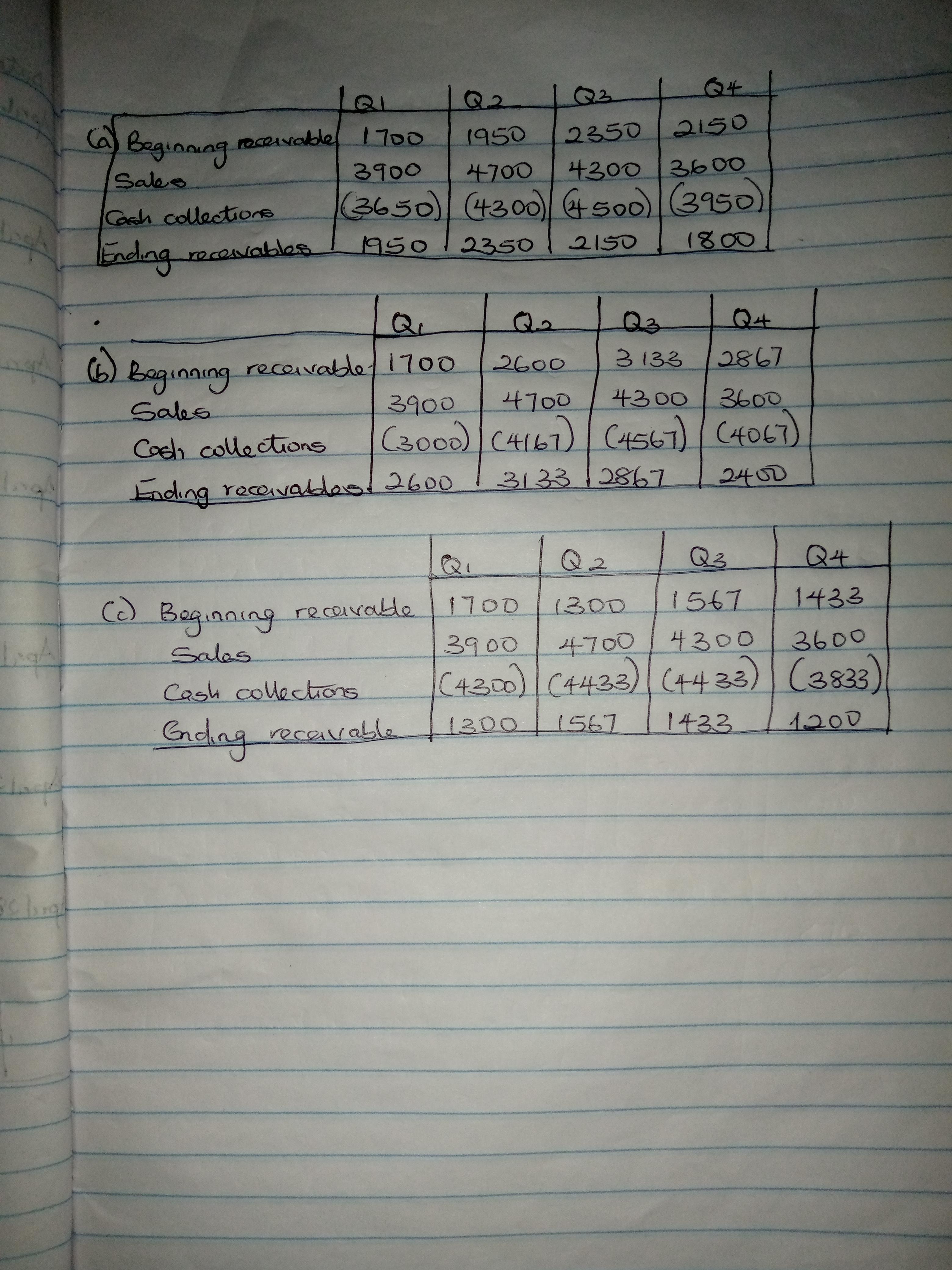

The cash collection was calculated as:

a. (90-45)/90 = 1/2

Q1 = 1700 + (1/2 × 3900)

= 1700 + 1950

= 3650

Q2 = 1950 + (1/2 × 4700)

= 1950 + 2350

= 4300

Q3 = 2350 + (1/2 × 4300)

= 2350 + 2150

= 4500

Q4 = 2150 + (1/2 × 3600)

= 2150 + 1800

= 3950

Check the attachments for further information.

Answer: $22.22

Explanation:

We can use the dividend discount model to solve for this.

The formula is,

P = D1 / r - g

Where,

D1 = the next dividend

r = the expected return

g = the growth rate.

We do not have the expected return but we can calculate for it using the old stock price and growth rate. Making it x we have,

28.5 = 0.5 / x - 0.075

28.5 (x - 0.075) = 0.5

x = 0.5 / 28.5 + 0.075

x = 0.09254385964

x = 9.25 %

Now that we have the expected return we can calculate the new stock price with the new growth rate,

P = 0.5 / 9.25% - 7%

P = 22.2222222222

P = $22.22

The new stock price is $22.22

105 km/hr is the same as 65.244 miles per hour. You can do this by doing unit conversions until you get the satisfied units. Then you multiply and reduce the fraction. In this case, the answer is 65.244 miles per hour.

Correct option is A

HOPE IT HELPS YOU

MARK ME BRAINLIEST

Answer:

b. Somaya just launched an online shoe company

d. A publishing company sells health-based curricula.

Explanation:

Pure goods are goods that are not associated with any services.

Pure services are services not associated with any physical goods.

I hope my answer helps you.