<span>It is backed by collateral, and in this case since it is a home mortgage, the collateral is your home. That means that if you don't pay your loan monthly payments on time or don't pay them at all, then they can take your home away and you can end up on the streets. That's why it is secured, it is secured for the bank, not for you.</span>

Answer:

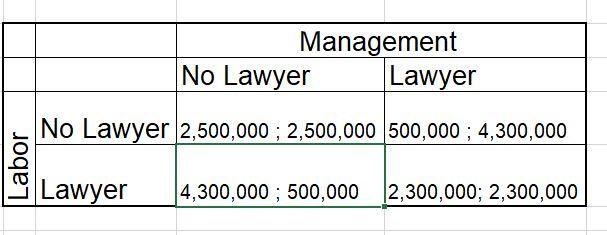

1. Please find it attached.

If both of them don't get lawyers they will each make half of the $5 million being $2.5 million a piece.

If one side hires a lawyer and the other doesn't, the side with the lawyer will win 0.9 of $5 million which is $4,500,000. However they would have paid the lawyer $200,000 so that payout drops to $4,500,000. The other would make 0.1 which is $500,000.

If they both get a lawyer they will each get half which is $2,500,000 but they would both have paid their lawyers $200,000 a piece so the net payout would be $2,300,000.

2. The Nash Equilibrium is the alternative that it would not serve either party to deviate from as it serves them both well. The Nash Equilibriums would be If both don't get a lawyer or if both get a lawyer.

3. Yes they would because without lawyers they would make more money as they would not have to pay the $200,000 in fees.

Answer:

Creative originator.

Explanation:

Tim is neither a project manager, because his web page was a personal project, and no other people were involved under his command, and his is not a godfather either.

He would be an entrepreneur if he had sold his web pages.

For the reasons above he is a creative originator: he essentially gave birth to a new work activity.

Answer:

$48,307

Explanation:

The carrying value is the value of the bond plus any unamortized premiums or less any unamortized discounts.

Government grants. If not showing the options would help