Answer:

The correct answer is option c.

Explanation:

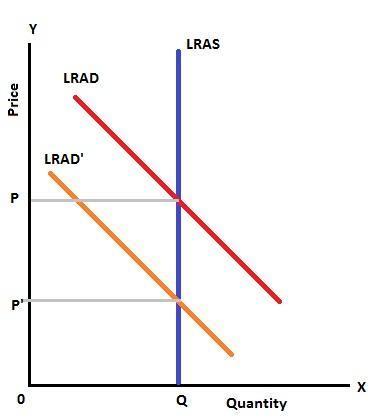

In an economy, in the long run, the aggregate supply is fixed. The aggregate supply curve is a vertical line. This is because, in the long run, supply remains unaffected by price level. The increase in product price is balanced by an increase in input prices. So the supply does not change with change in the price level.

In the long run, the supply changes with change in the availability of resources and change in technology. So when the aggregate demand declines, the demand curve shifts to the left. The equilibrium quantity remains the same but the price level declines.

It is also evident in the figure attached.

Answer:

Option B ⇒ The annual interest rate on Note A is 9.35% .

Explanation:

Note B has an accrued interest for six months during 2013: $220,000 x .08 x 6/12 = $8,800.

The remainder of the accrued interest, $7,200 ($16,000 - $8,800) was from Note A, which was held for seven months in 2013.

Therefore, we have the following: $132,000 x annual interest rate x 7/12 = $7,200.

Thus, the annual interest rate on Note A would be ($7,200/132,000) x 12/7 = 9.35%.

Option B ⇒ 9.35% is the correct answer.

The four common elements of an organization include (D) common purpose, coordinated effort, division of labor, and hierarchy of authority.

Explanation:

The organizational psychologist<u> Edgar Schein </u>proposed four common elements of an organization’s structure namely

-

<u>Common purpose

:</u>It refers to the clarity of the mission and vision.

- <u>Coordinated effort

:</u>Individualistic and group effort

- <u>Division of labor

:</u>Work specification for greater efficiency

- <u>Hierarchy of authority

:</u>Setting chain of commands

If we see from the point of view of a manager the day to day operations operations of an organization can be made successful by instilling a common purpose,which result in coordinated effort across the organization and then the work is allocated on the basis of the specialization of the staff and the hierarchy of authority is also defined

Answer:

Yes, he can buy stock in Apple.

Explanation:

Answer:

Maybe a loss in jobs?

Explanation: Because people who work for the oil company have to stop working idk