Is it a multiple choice question? Anyway, this is the definition of a limited partnership:

<span>A Limited Partnership is a partnership consisting of a general partner, who manages the business and has unlimited personal liability for the debts and obligations of the Limited Partnership, and a limited partner, who has limited liability but cannot participate in management.</span>

Answer:

Disobedience of the law or it may be ignorance

Explanation:

It may be that the kids didnt see the sign or it might be ignorance

A new fund offer (NFO) is the first-time subscription offer for a new scheme launched by asset management companies (AMCs). A new fund offer is launched in the market to raise capital from the public in order to buy securities like shares, govt. bonds etc. from the market.

In economic accounting, an asset is any aid owned or managed by using a business or an economic entity. It is whatever (tangible or intangible) may be used to produce a fine monetary fee. Belongings represent the price of ownership that can be transformed into cash (even though coins itself is also considered an asset). The stability sheet of a firm records the financial price of the property owned by that firm. It covers money and other valuables belonging to a person or to an enterprise. Belongings may be grouped into two essential lessons: tangible property and intangible belongings. Tangible property includes numerous subclasses, consisting of modern-day property and fixed property. present-day assets encompass coins, stock, and accounts receivable, while constant assets consist of land, buildings, and gadget. Intangible belongings are non-bodily resources and rights that have value to the firm because they give the firm an advantage inside the market. Intangible belongings include goodwill, copyrights, emblems, patents, laptop applications, and economic property, consisting of economic investments, bonds, and shares.

Learn more about asset here

brainly.com/question/25746199

#SPJ4

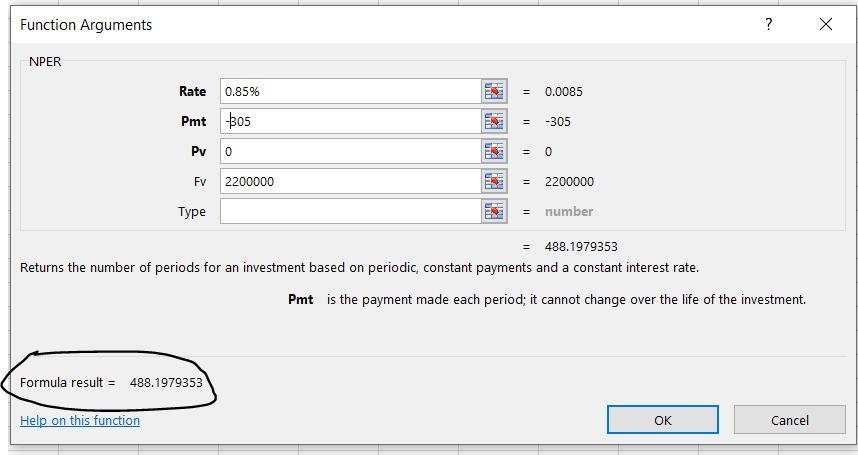

Answer: 40.7 years

Explanation:

You can use Excel to sold for this using the NPER function.

Rate = 10.2% / 12 months = 0.85%

Payment is $305 per month

Present value is $0

Future value is $2,200,000

Number of periods = 488.1979353

In years this is:

= 488.1979353 / 12

= 40.7 years