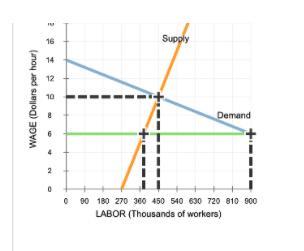

Answer:

The equilibrium hourly wage is the wage where the curve of supply of labor intersects with that of the demand for labor. The same goes for the equilibrium quantity of labor.

The equilibrium hourly wage is <u>$10</u>, and the equilibrium quantity of labor is <u>450 thousand workers</u>.

If a Senator introduces a minimum hourly wage, this is considered a <u>Price Floor. </u>

Price floors are prices that that the government mandates that one cannot charge below for a good or service. If there is a price floor on cake for instance, a person is not allowed to charge less than that price floor for cake. The Senator's bill is therefore saying that people should not be paid less than $6 an hour.

Answer:

About 84.2

Explanation:

8% of 78.00 = 6.24

78.00 + 6.24 = 84.24 (Around 84.2

apologies if wrong

Answer:

Click through rate

Explanation:

Click-through rate (CTR) are used to measure many of the decisions that go into a campaign, such as keyword selection and ad copy because the numbers of users who click on the advert link to the number of all total users who has either view the page of the advertisement and It is used to measure the success of an online advertising campaign for a website as well as how effective email campaigns are, by measuring or evaluating the numbers of people who actually saw the advert and click on the link of the advert that is why click through rate do not measure the performance of an advert campaign but rather useful to evaluate many of the decisions that go into a campaign.

Therefore the higher the click-through rate of an advert the more successful the advert has been in generating interest.

It can be C because it's accepting the risk to do it

But it can also be B because it's sharing the risk with everyone else

Answer:

Closing inventory = 54,000 units

Explanation:

<em>The difference between profit under variable costing and under absorption costing is simply the value of the change in inventory.</em>

<em>Usually, a decrease in inventory would cause profit under absorption costing to be lower . This is so because cost of goods sold would become higher leading to a lower profit</em>

Difference in profit = POAR × change inventory

POAR- fixed overhead cost per unit- $10,

Difference in profit - $120,000

let the change inventory be y

120,000 = 30 × y

y= 120,000/30

y = 4000 units

Inventory at the end = opening inventory + change inventory

= 50,000 + 4000

= 54,000 units

<em>Note; An increase in inventory will produce a higher profit using absorption costing. Hence, we added the change inventory to the opening inventory, to reflect an increase in inventory</em>