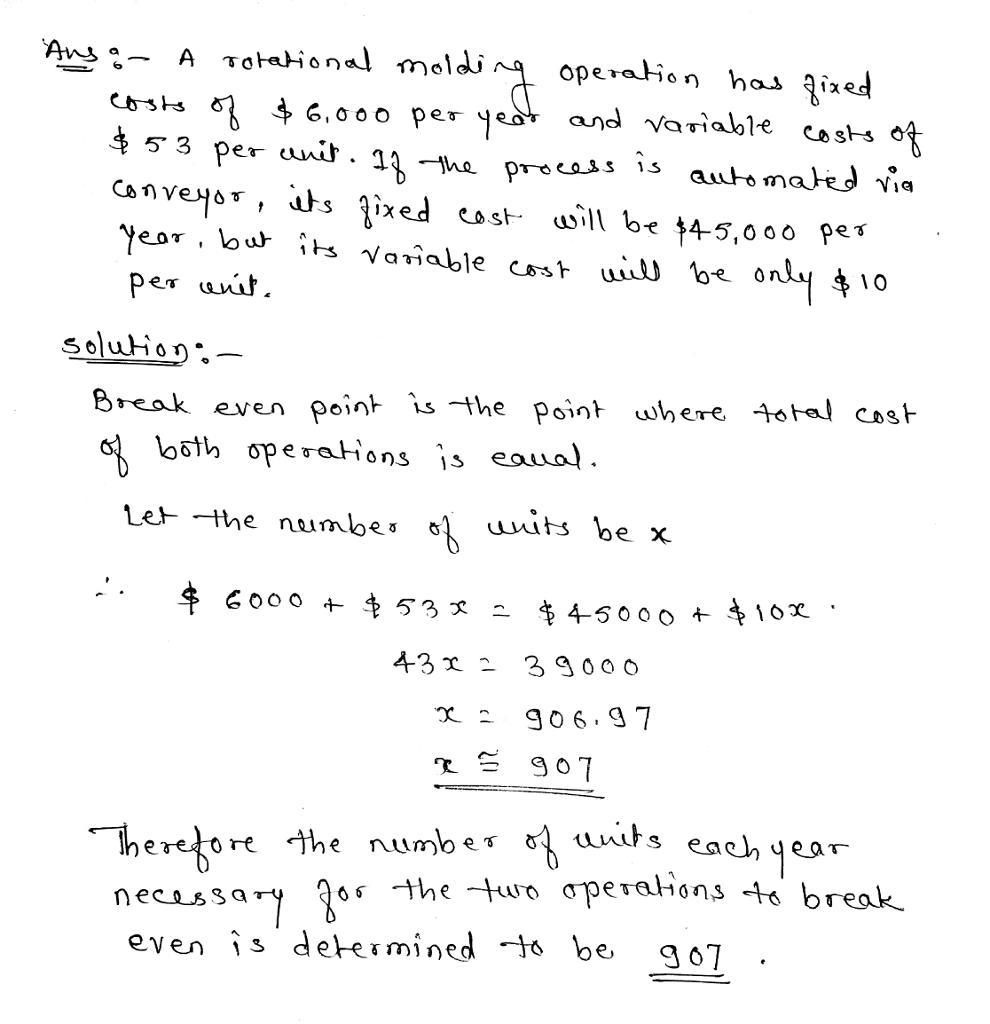

Answer:

Number of units required for the two operations to break even= 907 (approx)

Answer:

the same

Explanation:

it doesn't matter what was the original price elasticity of demand that the economist calculated in the first place, but if he/she changes the metrics, it wouldn't change the answer at all.

Price elasticity of demand measures the percentage change in the quantity demanded of the product over the percentage change in the price of the product.

The percentage change is measured in %, not in dollars, gallons, quarts, pints, tons, inches, etc.

If Ruskin receives a check and deposits it in its checking account, the float amount is $300,000.

<h3>What is the float amount?</h3>

The float amount is the amount that a customer's account reads in the bank at a particular point in time.

The float amount is usually briefly counted twice due to time gaps in registering a deposit and processing the paper checks.

Thus, if Ruskin receives a check and deposits it in its checking account, the float amount is $300,000.

Learn more about the float amount in the bank at brainly.com/question/24161262

#SPJ1

λ=3

, mu = 5

<u>Explanation</u>:

λ=3

mu = 5

states

0 - no customers

1- 1 customre

2 - 2 customers

Set up Equations

Rate of entry = Rate of exit

5P1 =3P0

5P2 + 3P0 = 5P1 + 3P1

3P1 = 5P2

P0 + P1 + P2 = 1

solve the above

1a) = 0 into P0 plus 1 into P1 plus 2 into P2

b) λ ( 1 minus P2) by λ = 1 - P2

c) change the paramater mu = 5 into 2 and solve a) again