Answer:

The answer is: YES

Explanation:

Hot Products is the legitimate owner of the patent for the manufacturing and commercialization of that fan motor. If Allied Electric wants to produce and use that specific fan motor they must come to a manufacturing licence agreement with Hot Products even thought the fan motor is used differently (one in ceiling fans and the other in air conditioners).

Answer: C.

Intercoms are a very useful system for businesses because, it allows the customers to just drive up an order from the machine rather than having to get out of the car and going into the restaurant establishment itself.

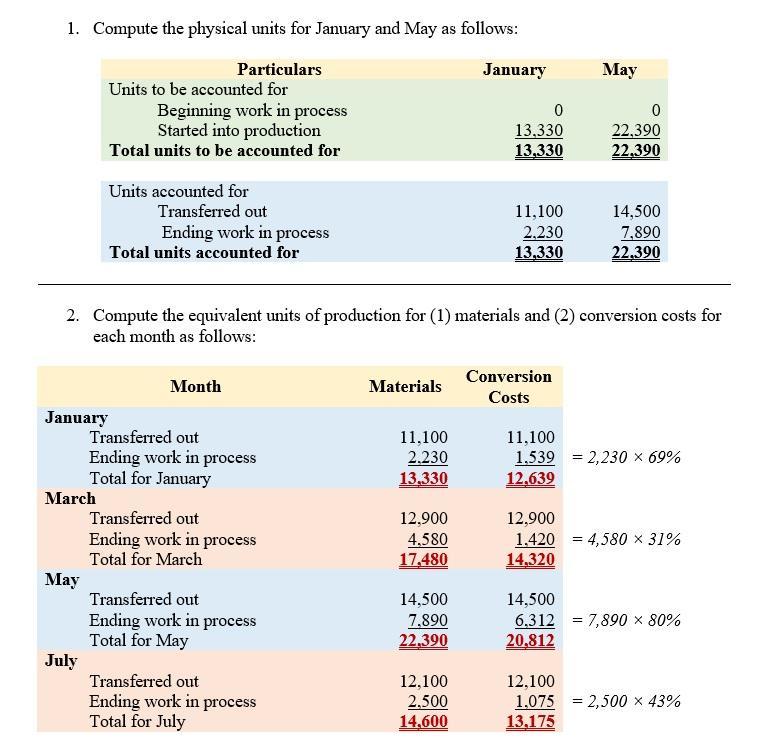

Answer:

Detailed step-wise solution is given below:

Answer:

D. A firm's weighted average cost of capital decreases as the firm's debt-equity ratio increases.

Answer:

E. Is the purpose realistic?

Explanation:

A purpose would be referred to as realistic, when it is backed by real evident reasons which determine the chances of happening or non happening of an event. It refers to realistic perception which is backed by logics, reasons and practicality rather than a desire, whim or an impulse.

In the given case, the company is going through a rough patch financially. In such a scenario, one of it's employees is desirous of pay raise and is considering to compose and send a message for the same object.

With available facts and situation apparent to the employee, it would first realistically seek an answer to the question, whether realistically his demand would be met, given the situation.

The employee needs to weigh in the pros and cons and decide if it would be the right time to send such a message and the possibility of how such a demand would be responded/reacted to.