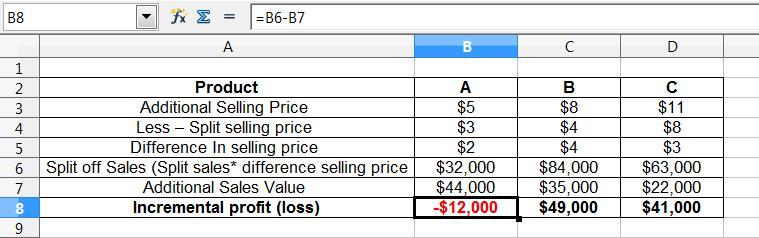

Answer:

The incremental profit (loss) for each product is:

A = $-12,000

B = $49,000

C = $41,000

Explanation:

Split off Point: The split off point is that point in which joint products treated separately and sell them as a unique product.

Incremental Cash flow: The incremental cash flow is that cash flow which show the difference between the split off sales and normal sales.

Here, incremental means that if split off sales is greater than normal sales than firm is earning profit else the firm will suffer loss.

Steps to compute the incremental cash flows for each products:

Step 1: First write Additional selling price of all three products

Step 2: Than write the Split off selling price of all three products

Step 3: Now take the difference of selling price

Step 4: After that, multiply step 3 with split off sales

Step 5: Than write the additional sales

Step 6: Compare the two sales and analyse whether firm earns profits or suffer a loss, and finally the increment cash flows come.

The calculation is done in attachment sheet.

Thus, the incremental profit (loss) for each product is:

A = $-12,000

B = $49,000

C = $41,000